A Traditional Individual Retirement Account (IRA) is a tax-advantaged retirement savings account that enables you to contribute pre-tax dollars to an investment account. These contributions may reduce your taxable income in the year they are made, while the earnings within the account grow tax-deferred until withdrawal. Upon distribution, typically in retirement, the funds are taxed as ordinary income. This structure is particularly beneficial for individuals who anticipate being in a lower tax bracket during retirement than during their working years. However, the tax advantages of a Traditional IRA depend on future tax rates and your personal financial circumstances, making it essential to assess your projected income and tax bracket in retirement. For additional questions or personalized guidance, schedule a consultation with us.

Contributions

Eligibility

If you receive taxable compensation, commonly referred to as earned income, you are eligible to contribute to a Traditional IRA (no age limit). Earned income includes wages, salaries, commissions, tips, bonuses, or net income from self-employment. It’s income generated through active personal effort or labor. In contrast, passive income – often classified as unearned income – does not qualify for a Traditional IRA contribution. Examples of unearned income include interest accrued from savings accounts, dividends paid on investments, capital gains realized from the sale of assets, unemployment compensation, Social Security benefits, and similar receipts.

In some instances, those without personal earned income can still contribute to a Traditional IRA: if you are married and file a joint tax return with a spouse who has earned income, then you may still contribute through what is known as a spousal IRA. This provision offers a valuable opportunity for married couples to bolster their retirement savings, even when one spouse does not participate in the workforce.

Regarding the mechanics of contributions, the Internal Revenue Service stipulates that, with the exception of rollover contributions—transfers from another qualified retirement account—all contributions must be made in cash. Contributions in the form of property, securities, or other non-monetary assets are not permitted.

Annual Limits

The amount you can contribute to a Traditional IRA each year is limited to the lesser of two figures: your taxable compensation (earned income) for the tax year or the annual contribution limit established by the Internal Revenue Service (IRS), as detailed below.

↳ For Tax Year 2025

| Yearly Contribution Limit | Catch-Up Contribution (age 50+) |

|---|---|

$7,000 |

+ $1,000 |

-

The additional $1,000 allowed for those age 50 and above is known as a “catch-up” contribution, designed to help older savers bolster their retirement funds as they near retirement age.

-

Important Note: these figures reflect the total contribution limit across all your Traditional and Roth IRAs combined for a given tax year, excluding rollovers.

↳ For Tax Year 2024

| Yearly Contribution Limit | Catch-Up Contribution (age 50+) |

|---|---|

$7,000 |

+ $1,000 |

-

The additional $1,000 allowed for those age 50 and above is known as a “catch-up” contribution, designed to help older savers bolster their retirement funds as they near retirement age.

-

Important Note: these figures reflect the total contribution limit across all your Traditional and Roth IRAs combined for a given tax year, excluding rollovers.

↳ For Tax Year 2023

| Yearly Contribution Limit | Catch-Up Contribution (age 50+) |

|---|---|

$6,500 |

+ $1,000 |

-

The additional $1,000 allowed for those age 50 and above is known as a “catch-up” contribution, designed to help older savers bolster their retirement funds as they near retirement age.

-

Important Note: these figures reflect the total contribution limit across all your Traditional and Roth IRAs combined for a given tax year, excluding rollovers.

Deduction Limits

The ability to claim a deduction for contributions to a Traditional IRA on your federal income tax return depends on your Modified Adjusted Gross Income (MAGI) and whether you or your spouse are covered by an employer retirement plan. If your MAGI exceeds certain thresholds—determined by your filing status—the deduction may be reduced or eliminated entirely. The specific limits for this deduction are outlined below.

↳For Tax Year 2025

| Filing Status | And if your MAGI is... | Then you can take... |

|---|---|---|

| Married filing jointly and you are covered by a plan at work | ≤ $126,000 | Full Deduction |

| Between $126,000 & $146,000 | Partial Deduction | |

| ≥ $146,000 | No Deduction | |

| Married filing jointly and your spouse is covered by a plan at work | ≤ $236,000 | Full Deduction |

| Between $236,000 & $246,000 | Partial Deduction | |

| ≥ $246,000 | No Deduction | |

| Single or HOH and you are covered by a plan at work | ≤ $79,000 | Full Deduction |

| Between $79,000 & $89,000 | Partial Deduction | |

| ≥ $89,000 | No Deduction | |

| Single, HOH, Qualifying Widow(er), Married filing jointly and neither spouse is covered by a plan at work. | Any Amount | Full Deduction |

↳For Tax Year 2024

| Filing Status | And if your MAGI is... | Then you can take... |

|---|---|---|

| Married filing jointly and you are covered by a plan at work | ≤ $123,000 | Full Deduction |

| Between $123,000 & $143,000 | Partial Deduction | |

| ≥ $143,000 | No Deduction | |

| Married filing jointly and your spouse is covered by a plan at work | ≤ $230,000 | Full Deduction |

| Between $230,000 & $240,000 | Partial Deduction | |

| ≥ $240,000 | No Deduction | |

| Single or HOH and you are covered by a plan at work | ≤ $77,000 | Full Deduction |

| Between $77,000 & $87,000 | Partial Deduction | |

| ≥ $87,000 | No Deduction | |

| Single, HOH, Qualifying Widow(er), Married filing jointly and neither spouse is covered by a plan at work. | Any Amount | Full Deduction |

What is my MAGI?

For many people, their Adjusted Gross Income (AGI) will be similar to or the same as their Modified Adjusted Gross Income (MAGI), but MAGI often involves adding back certain deductions to AGI for specific purposes, like figuring out Traditional IRA deduction limits. Here’s a quick snapshot of how to calculate your MAGI:

- Calculate Your Gross income

- Your gross income is all the money you earn in a year from any source—think salary, capital gains, interest, retirement income, unemployment benefits, and more.

- Figure Out Your Adjusted Gross Income

- Your AGI starts with gross income, then subtracts certain adjustments, like contributions to a traditional IRA or other qualified retirement plans, HSA contributions, half of self-employment tax, self-employed health insurance premiums, student loan interest, educator expenses, and other eligible deductions as outlined by the IRS.

- Add Back Certain Deductions for MAGI

- To get MAGI, you add back things like the student loan interest deduction, foreign earned income and housing exclusions, foreign housing deduction, excluded savings bond interest, and excluded employer adoption benefits

This will give you a rough idea of your MAGI. But since tax rules can get tricky, it’s a good idea to check with a tax advisor for an exact number.

Contribution Deadline

Contributions to a Traditional IRA can be made at any time throughout the year—spanning January 1 to December 31—or up to the due date of your federal income tax return (around April 15th), not including extensions. This flexibility lets you plan your contributions strategically, whether you prefer to invest early in the year or wait until you’ve finalized your tax situation. For instance, the filing deadline for 2024 tax returns is expected to be April 15, 2025. You have until that date to make a Traditional IRA contribution designated for the 2024 tax year.

Rollovers Into: Traditional IRA

A rollover is a tax-free distribution of funds from one retirement plan to another eligible retirement plan, with the contribution to the second plan referred to as a “rollover contribution.” There are several compelling reasons to consider rolling funds from another retirement plan into a Traditional IRA. These include simplifying account management, accessing a broader range of investment options, and potentially benefiting from lower fees in the Traditional IRA.

↳Rollover Chart: Which Retirement Accounts Are Allowed To Be Rolled Into A Traditional IRA

| Type of Account | Allowed? |

|---|---|

| Roth IRA | No |

| Traditional IRA | Yes ₍₂₎ |

| SIMPLE IRA | Yes, after two year ₍₂₎ |

| SEP IRA | Yes ₍₂₎ |

| Governmental 457(b) Plan | Yes |

| Qualified Plan ₍₁₎ (pre-tax) | Yes |

| 403(b) Plan (pre-tax) | Yes |

| Designated Roth Account (401(k), 403(b), or 457(b)) | No |

Additional info: (1)(2)

(1) – Qualified plans include profit-sharing, 401(k), money purchase, and defined benefit plans. (2) – Only one rollover in any 12-month period.

Additional info: (1)(2)

↳ Rollover a Qualified Plan Into a Traditional IRA

You may choose to roll over the pre-tax portion of a qualified retirement plan (e.g., 401(k), profit-sharing plan) into a Traditional IRA after separating from service with your employer. A Traditional IRA typically offers lower fees and a broader range of investment options compared to many qualified plans.

↳ More on Rollovers: Individuals Can Perform a Rollover in The Following Ways

- Direct rollover – An account holder must request instructions from their plan administrator. Typically, a check is made payable to the new 401(k) or IRA custodian (e.g., “Fidelity Investments FBO [Your Name]”) and sent directly to the new plan. No taxes are withheld from the transfer amount because the funds do not pass through the individual’s hands.

- Trustee-to-trustee transfer – The trustee or custodian of one plan transfers the rollover amount directly to the trustee or custodian of another plan. This is common for IRA-to-IRA transfers. No taxes are withheld, and the individual does not take possession of the funds.

- 60-day rollover – If a distribution from an IRA or retirement plan is paid directly to you (e.g., a check in your name), you can deposit all or a portion of it into an eligible retirement plan within 60 days. For distributions from a retirement plan like a 401(k), taxes (typically 20%) are withheld, so you’ll need to use other funds to roll over the full pre-tax amount. For IRA distributions, taxes are not automatically withheld unless requested.

- Note: Only one IRA-to-IRA 60-day rollover is allowed per 12-month period (this limit does not apply to direct rollovers, trustee-to-trustee transfers, or rollovers involving employer plans).

Investments

Type of Investments

When you establish a Traditional IRA, the range of investment options available to you depends on the brokerage firm, bank, or financial institution you choose as your custodian. (For our recommendation on a trusted brokerage, please refer to the Recommended Brokerage page.) These custodians typically offer a variety of investment vehicles to help you build a diversified retirement portfolio tailored to your financial goals. Most brokerage firms and banks provide the following investment options within a Traditional IRA:

- Exchange traded funds (ETFs)

- Money market funds

- Mutual funds

- Index funds

- Individual bonds

- Individual stocks

Investment Options In Self-Directed Traditional IRAs

Self-directed Traditional IRAs offer a broader spectrum of investment choices but come with increased risks and responsibilities. Depending on the self-directed IRA custodian, these investments may include real estate, gold, business partnerships, cryptocurrency, and other alternative assets. While this flexibility provides opportunities, it requires careful due diligence due to higher risks, potential illiquidity, and complex IRS rules, such as prohibitions on self-dealing. Custodians may also charge higher fees for managing these assets, and valuation can be less transparent.

Prohibited Investments

IRS rules prohibit Traditional IRA funds from being invested in certain assets, including life insurance contracts, collectibles (such as art, antiques, stamps, or certain coins), S corporation stock, and other restricted investments as defined by tax laws. If you invest your Traditional IRA in any prohibited asset, the amount invested is treated as a taxable distribution in the year of the investment. This could result in income taxes on the distribution, and if you are under age 59½, you may also face a 10% early withdrawal penalty.

Prohibited Transactions (self-dealing)

Prohibited transactions involve certain improper dealings or transactions between a Traditional IRA and yourself, your beneficiary, or any disqualified person, as defined by IRS rules. Unlike prohibited investments, these transactions do not restrict the types of assets you can hold in your Traditional IRA but instead limit interactions that could benefit disqualified persons or involve self-dealing. If a prohibited transaction occurs, the Traditional IRA is treated as distributed on January 1 of the tax year in which the transaction took place, resulting in the loss of its tax-advantaged status. The fair market value of the IRA becomes taxable, and if you are under age 59½, you may also face a 10% early withdrawal penalty.

Who is a disqualified person?

- A family member, such as a spouse, parent, child, or other ancestor/descendant

- A fiduciary of the Traditional IRA

- A person with discretionary control over your Traditional IRA

- A person providing fee-based investment advice for your Traditional IRA

- A person responsible for administering your Traditional IRA

Examples Of Prohibited Transactions

When managing a self-directed Traditional IRA, it’s crucial to avoid prohibited transactions due to their significant and severe tax consequences. Given the variety of prohibited transactions, here are a few examples to enhance understanding:

(1) Selling property to your Traditional IRA – It is a prohibited transaction if you sell property (owned by you or a disqualified person) to your Traditional IRA—for example, purchasing your mother’s house for the account.

(2) Buying property for personal use – It is a prohibited transaction if you buy property within your Traditional IRA that you or a disqualified person use for personal benefit—for example, acquiring a condo to rent but also vacationing there.

(3) Making certain loans – It is a prohibited transaction if you make a loan from your Traditional IRA to yourself or a disqualified person—for example, lending money to your business or your child.

(4) Using the Traditional IRA as loan collateral – It is a prohibited transaction if you use your Traditional IRA as collateral for a loan.

Distributions

Before Age 59½

You can withdraw funds from your Traditional IRA at any time; however, such withdrawals are generally taxable as ordinary income in the year of withdrawal. If you are under age 59½, you may also be subject to a 10% early withdrawal penalty, unless an exception applies (detailed in the tab below).

Exceptions to the 10% penalty rule

You may avoid the 10% penalty if one of the following IRS-approved exceptions applies:

- Qualified Birth or Adoption Expenses: Distributions up to $5,000 per parent for expenses related to the birth or adoption of a child, if taken within one year of the event.

- Disability or Death: Total and permanent disability of the account holder (as defined by IRS rules under Section 72(m)(7)) or distributions following the account holder’s death.

- Qualified Higher Education Expenses: Expenses for yourself, your spouse, your children, or grandchildren, covering tuition, fees, books, supplies, and room and board (if the student is enrolled at least half-time).

- First-Time Home Purchase: Distributions up to a $10,000 lifetime limit for qualified first-time homebuyer expenses, applicable to yourself, your spouse, or your dependents.

- Unreimbursed Medical Expenses: Expenses exceeding 7.5% of your Adjusted Gross Income (AGI) for the year, covering medical care for yourself, your spouse, or dependents.

- Health Insurance Premiums During Unemployment: Premiums paid for health insurance while unemployed for at least 12 consecutive weeks, applicable to yourself, your spouse, or dependents.

- Other IRS-Approved Exceptions: These include substantially equal periodic payments (SEPP) under Section 72(t), distributions to qualified military reservists called to active duty, or other specific circumstances outlined by the IRS.

After Age 59½

You can withdraw funds from your Traditional IRA at any time; however, such withdrawals are generally taxable as ordinary income in the year of withdrawal. No early withdrawal penalty after age 59½. After age 73 though, you are required to take minimum distributions (RMDs) annually to avoid additional penalties.

Required Minimum Distributions (RMDs)

You must begin taking Required Minimum Distributions (RMDs) from your Traditional IRA by April 1 of the year following the year in which you turn 73, regardless of employment status. Subsequent RMDs must be taken by December 31 of each year thereafter. The RMD amount is generally calculated by dividing the account balance of your Traditional IRA(s) as of December 31 of the preceding year by the life expectancy factor corresponding to your age in the IRS Uniform Lifetime Table.

If you have multiple Traditional IRAs, you must calculate the RMD for each Traditional IRA separately each year. However, you may aggregate the total RMD amounts and withdraw the sum from one Traditional IRA or distribute portions from each Traditional IRA, as long as the total annual RMD minimum is withdrawn. You may take your RMD in any number of distributions throughout the year, provided the full amount is withdrawn by the deadline.

If the distributions received in any year are less than the required RMD, you are subject to a severe excise tax on the undistributed amount.

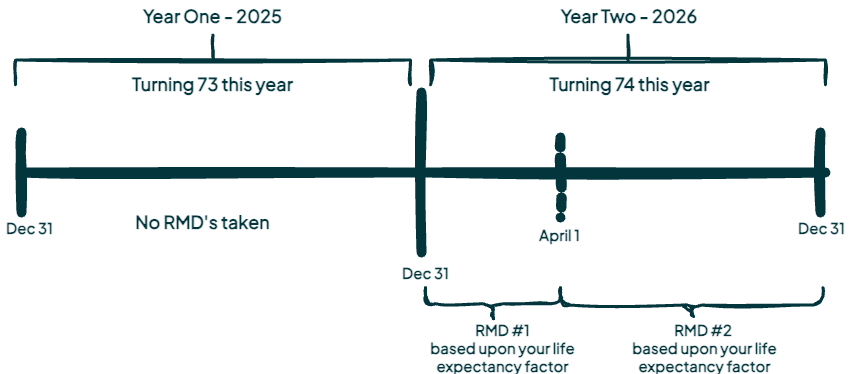

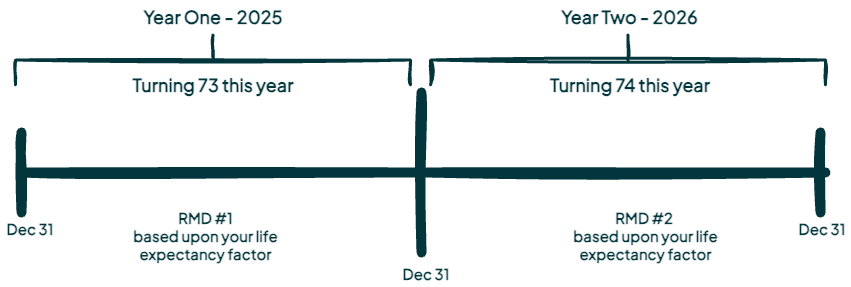

Turning 73? See how your first RMD timeline may work

Option One –Take your first RMD by April 1 of the following year and your second RMD by December 31 of that same year. This results in two RMDs in one year, potentially pushing you into a higher tax bracket.

Option Two – Take your first RMD in the year you turn 73 (by December 31) and your second RMD the following year by December 31. This splits the RMDs across two years, reducing the likelihood of entering a higher tax bracket compared to Option One.

Qualified Charitable Distributions (QCD)

If you are age 70½ or older, you can transfer up to $108,000 annually (for 2025) directly from your Traditional IRA to a qualified charity as a Qualified Charitable Distribution (QCD), avoiding federal income tax on the distribution. This amount is excluded from your federal taxable income, though you cannot claim an additional charitable deduction since the QCD is already tax-free. The funds must be transferred directly from your IRA custodian to the charity—distributions paid to you first do not qualify.

QCDs can satisfy your Required Minimum Distribution (RMD) if applicable, making them a tax-efficient way to support charities while minimizing taxable income. However, it is important to note the ‘first-dollars-out’ rule: any withdrawal from a Traditional IRA in a year you are subject to an RMD is deemed to satisfy the RMD first, which can create timing issues if you want to use QCDs to reduce taxable income by your RMD amount. To optimize a QCD, make your QCD directly from your Traditional IRA to a qualified charity first (typically at the beginning of the year) so they count towards your RMD before taking additional distributions, if desired.

Finally, QCDs must be completed by December 31, as they apply only to the current calendar year.

Eligible Charitable Organizations

The recipient must be a qualified charitable organization recognized by the IRS under Section 501(c)(3) of the Internal Revenue Code as a public charity, such as churches, universities, hospitals, or community nonprofits. Excluded entities include private foundations, donor-advised funds, supporting organizations, and most foreign charities (unless U.S.-based affiliates).

To confirm eligibility, use the IRS Tax Exempt Organization Search tool at IRS.gov to verify the charity’s 501(c)(3) status and public charity classification.

Rollovers Out: From Traditional IRA

A rollover is a tax-free distribution of funds from one retirement plan to another eligible retirement plan, with the contribution to the second plan termed a “rollover contribution.” Rolling funds out of a Traditional IRA may offer benefits such as consolidating accounts for simpler management, accessing a broader range of investment options, and potentially reducing fees, depending on the receiving plan’s structure. However, tax considerations can vary based on your financial situation, including whether the rollover involves a conversion to a Roth account, which triggers taxable income.

↳ Rollover Chart: Which Retirement Accounts Are Allowed To Accept A Traditional IRA Rollover

| Type of Account | Allowed? |

|---|---|

| Roth IRA | Yes ₍₃₎ |

| Traditional IRA | Yes ₍₂₎ |

| SIMPLE IRA | Yes, after two years ₍₂₎ |

| SEP IRA | Yes ₍₂₎ |

| Governmental 457(b) Plan | Yes ₍₄₎ |

| Qualified Plan ₍₁₎ (pre-tax) | Yes |

| 403(b) Plan (pre-tax) | Yes |

| Designated Roth Account (401(k), 403(b), or 457(b)) | No |

Additional info:(1)(2)(3)(4)

(1) – Qualified plans include profit-sharing, 401(k), money purchase, and defined benefit plans. (2) – Only one rollover in any 12-month period. (3) – Must include in income (4) – Must have a seperate account

Additional info:(1)(2)(3)(4)

↳ Rollover Traditional IRA to Roth IRA

You might consider rolling over funds from a Traditional IRA to a Roth IRA in a year when your income is lower, as the rollover amount—known as a Roth conversion—is treated as taxable ordinary income in the year of the conversion. By timing the conversion during a low-income period, you may “lock in” a lower tax rate, potentially reducing your overall tax burden. Once in the Roth IRA, the funds grow tax-free, Required Minimum Distributions (RMDs) are not required during your lifetime, and qualified distributions are tax-free.

↳ Traditional IRA To A Qualified Retirement Plan (e.g., 401(k))

May be advantageous in certain situations. These include delaying Required Minimum Distributions (RMDs) if you’re still working and the plan allows it, or reducing your Traditional IRA balance to zero to enable a backdoor Roth IRA contribution.

Important Note: not all plans accept incoming rollovers, so you’d need to verify eligibility with the plan administrator.

↳ More On Rollovers: Individuals can perform a rollover in the following ways

- Direct rollover – An account holder must request instructions from their plan administrator. Typically, a check is made payable to the new 401(k) or IRA custodian (e.g., “Fidelity Investments FBO [Your Name]”) and sent directly to the new plan. No taxes are withheld from the transfer amount because the funds do not pass through the individual’s hands.

- Trustee-to-trustee transfer – The trustee or custodian of one plan transfers the rollover amount directly to the trustee or custodian of another plan. This is common for IRA-to-IRA transfers. No taxes are withheld, and the individual does not take possession of the funds.

- 60-day rollover – If a distribution from an IRA or retirement plan is paid directly to you (e.g., a check in your name), you can deposit all or a portion of it into an eligible retirement plan within 60 days. For distributions from a retirement plan like a 401(k), taxes (typically 20%) are withheld, so you’ll need to use other funds to roll over the full pre-tax amount. For IRA distributions, taxes are not automatically withheld unless requested.

- Note: Only one IRA-to-IRA 60-day rollover is allowed per 12-month period (this limit does not apply to direct rollovers, trustee-to-trustee transfers, or rollovers involving employer plans).

Inheritance and Death

When you pass away, your Traditional IRA is transferred to the beneficiary or beneficiaries you designated. The account doesn’t disappear—it becomes an inherited IRA. What happens next depends on who inherits it. A surviving spouse has the most flexibility, while other beneficiaries, such as children or non-spouse individuals, generally must withdraw the entire balance within 10 years.

All withdrawals from a Traditional IRA are taxed as ordinary income to the beneficiary, and there is no step-up in basis. If no beneficiary was named, the IRA becomes part of your estate, which can complicate both distribution and taxation. Overall, an inherited Traditional IRA continues to grow tax-deferred until the funds are distributed according to IRS rules. Please refer to the inherited IRA page for more information on distribution options.

FAQs

What are the benefits / drawbacks of a Traditional IRA?

Benefits

- Tax-deductible contributions (subject to income limits based on MAGI and filing status), offering an immediate reduction in taxable income.

- Tax-deferred growth, allowing dividends, interest, and investment changes to accumulate without incurring a tax liability until withdrawal.

- Easy to set up, with broad availability through banks and brokerage firms.

- Anyone with taxable earned income can contribute, subject to annual limits

Drawbacks

- If you take a withdrawal before age 59½ (unless you qualify for specific IRS exceptions, as outlined), you may be subject to a 10% early withdrawal penalty.

- Contribution limits are relatively low

- Required Minimum Distributions (RMDs) must begin at age 73, regardless of financial need, and distributions are taxed as ordinary income.

Who can contribute to a Traditional IRA?

How much can I contribute to a Traditional IRA?

Contribution limits are set every year by the IRS and are tied to cost-of-living adjustments. You can contribute up to the annual contribution limit. Refer to the contribution (limits) section for more details.

Can my non-working spouse contribute to a Traditional IRA?

Yes, a spouse without taxable earned income can contribute to their own Traditional IRA, up to the annual contribution limit. However, you and your spouse must file a joint tax return, and the total contributions for both spouses must not exceed the working spouse’s taxable earned income. This type of contribution is known as a spousal IRA.

What happens if I contribute too much to my Traditional IRA?

Errors can occur, and you may inadvertently contribute more than the allowable amount to your Traditional IRA. It is important to correct this as soon as possible, as excess contributions are subject to a 6% excise tax each year they remain in the IRA. Below are some options to fix it:

(1) Remove Excess Before the Tax Filing Deadline – To avoid the 6% excise tax, you can remove your excess contributions, along with any net income attributable to them, before the federal income tax filing deadline—typically April 15 (or the next business day if April 15 falls on a weekend or holiday). The IRS will treat the contribution as if it never occurred. However, the net income attributable to the excess contribution will be taxed as ordinary income in the year of removal. The net income is calculated as:

- Net Income = Excess to be removed x ((Adjusted Closing Balance – Adjusted Opening Balance) / Adjusted Opening Balance)

If you identify the error after filing your taxes, you can still withdraw the excess contribution and net income, and submit an amended tax return, up to 6 months after the original filing deadline (typically October 15). The same rules apply: no additional 6% excise tax, but the net income is taxed as ordinary income.

(2) Carry Over Excess Amount – You will need to pay the 6% excise tax, but you can apply the excess contribution toward the next year’s contribution limit, up to the annual limit. Be aware you will continue to pay a 6% excise tax each year the excess amount remains in the IRA until it is fully applied to future contribution limits.

(3) Withdraw Excess Amount Later – If you cannot withdraw the excess contribution by the tax filing deadline or within 6 months of filing, you can still withdraw it later. However, you will pay the 6% excise tax each year the excess amount remains in your Traditional IRA.

When must I withdraw my funds from my Traditional IRA?

You are required to begin taking Required Minimum Distributions (RMDs) from your Traditional IRA by April 1 of the year following the year in which you turn 73, regardless of your employment status. Note that you can withdraw funds from your Traditional IRA at any time before age 73, but such withdrawals may be subject to income taxes and, if under age 59½, a 10% early withdrawal penalty unless an exception applies.