As you journey through life’s milestones—starting a family, purchasing a home, or preparing for retirement—life insurance often emerges as a vital safeguard. This financial tool delivers peace of mind by ensuring your loved ones remain financially secure if you pass away unexpectedly. Yet, its complexity can make selecting the right policy challenging, and a misstep might conflict with your financial objectives. To choose wisely, you must grasp the essentials of life insurance, including its financial commitments and the trade-offs between policy types. If uncertainty lingers about the best option for your needs, consider a consultation with TrustTas Capital for expert, personalized guidance tailored to your circumstances.

Overview

Life insurance serves as an effective financial planning tool, with over half of Americans maintaining some form of coverage to protect their loved ones, underscoring its widespread adoption for financial security. The necessity of life insurance, however, depends on individual circumstances, including income, outstanding debts, the number of dependents, and long-term financial goals.

For individuals with a spouse, children, or others reliant on their income, life insurance acts as an essential safety net, shielding them from financial distress in the event of the insured’s untimely passing. Conversely, those who are single, without dependents, and possess adequate savings or assets to meet future expenses may find minimal or no coverage more appropriate for their needs.

When you opt to purchase life insurance, you enter into a formal legal contract with an insurance provider. Under this agreement, the insurer pledges to pay a death benefit to your designated beneficiary upon your passing, while you commit to paying regular premiums to keep the policy active. This arrangement ensures that the promised protection remains available to your loved ones when it is most critical.

Types of Life Insurance

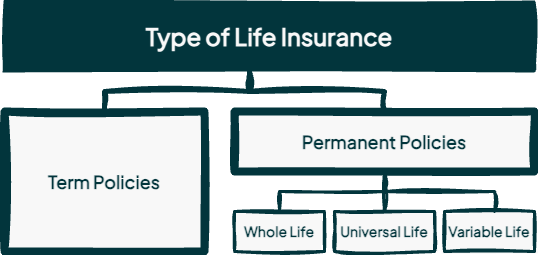

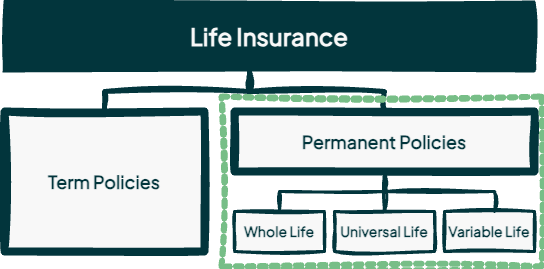

Life insurance policies come in a variety of forms, but they can be broadly categorized into two primary types—term and permanent—each designed to serve distinct financial purposes and strategies. Understanding the fundamental differences between these two categories is essential for selecting coverage that aligns with your goals, whether you’re seeking temporary protection or lifelong security.

Life insurance policies come in a variety of forms, but they can be broadly categorized into two primary types—term and permanent—each designed to serve distinct financial purposes and strategies. Understanding the fundamental differences between these two categories is essential for selecting coverage that aligns with your goals, whether you’re seeking temporary protection or lifelong security.

Term life insurance provides coverage for a specified period, making it an ideal choice for those who need affordable protection during specific high-risk periods—like raising a family or paying off a mortgage—after which the policy expires unless renewed or converted. In contrast, permanent life insurance offers lifelong coverage, ensuring a death benefit is paid out whenever the insured passes, often accompanied by a cash value component that grows over time.

By exploring these options, you can better determine which policy type best supports your financial strategy, providing peace of mind for your loved ones while fitting seamlessly into your broader planning objectives.

Which Policy Type Should I Buy…

Buy Term, Invest the Rest

When deciding between term and permanent life insurance, the choice often hinges on your unique financial goals and circumstances. For most clients focused on securing death benefit protection, we recommend term life insurance as the optimal choice, unless your primary aim is estate planning or leaving a legacy, where permanent insurance may be more suitable.

Term life insurance offers distinct advantages that make it an appealing option for many. First, its simplicity ensures transparency—we advocate investing only in products you fully understand, making term a straightforward and accessible choice. Second, it provides a dependable financial safety net for your loved ones in the event of your untimely passing, without the complexities of the cash value features found in permanent policies. Third, term life insurance is significantly more affordable than permanent coverage, enabling a strategic approach known as “buy term, invest the rest.”

The “buy term, invest the rest” strategy involves opting for a cost-effective term policy—for instance, one costing $50 per month—over a permanent policy with an equivalent death benefit, which might cost around $450 monthly. The $400 monthly savings can then be redirected into investments such as stocks, bonds, or retirement accounts. Over time, these investments have the potential to grow substantially, providing greater financial flexibility and security compared to the more restrictive framework of a permanent policy.

Coverage Analysis

One of the most critical questions you’ll encounter when considering life insurance is: how much coverage do you truly need? Without thorough evaluation, you may be influenced to purchase excess coverage that exceeds your financial goals and personal circumstances, potentially placing undue strain on your budget. Conversely, insufficient coverage could leave your loved ones financially exposed in the event of your passing.

Determining the appropriate coverage amount is less about adhering to a strict formula and more about a thoughtful, strategic assessment that considers your financial situation, family needs, and long-term aspirations. At TrustTas Capital, we advocate a holistic methodology, factoring in your unique lifestyle, debts, income, and future objectives to determine an optimal coverage level that balances security and peace of mind.

Tabbed below, we present various methods to estimate your coverage requirements, each offering distinct advantages and limitations. We recommend integrating these approaches to develop a comprehensive coverage range, ultimately customizing the decision to align with your family’s specific needs and financial vision.

↳ Manually Calculate

You can estimate your life insurance coverage needs by methodically comparing your future financial obligations to your available liquid assets, using a simple formula to guide your decision:

- Coverage Needed = Financial Obligations – Liquid assets

How to do the calculation? –Below are the detailed steps to conduct this manual calculation, ensuring you account for essential financial factors to determine a realistic coverage amount that aligns with your family’s needs and financial objectives.

Step 1: Total Your Financial Obligations – Start by calculating the full scope of your financial responsibilities, which may include:

- Income Replacement: Multiply your current annual income by the number of years you wish to replace it (e.g., $75,000 × 10 years = $750,000).

- Remaining Mortgage Balance: Include the outstanding amount on your home loan.

- Outstanding Debts: Sum all debts, such as credit card balances, car loans, or personal loans.

- Estimated Funeral Costs: Account for expenses, typically ranging from $10,000 to $15,000.

- Cost to Replace Stay-at-Home Parent Services: If applicable, estimate the annual cost of services like childcare or household management (e.g., $30,000/year × 10 years = $300,000).

- Future College Expenses (Optional): Estimate costs for your children’s education, if relevant (e.g., $50,000 per child).

Step 2: Total Your Liquid Assets –Next, assess the liquid assets currently available to offset these obligations, including:

- Savings and Checking Account Balances: Total funds in accessible accounts.

- Non-Retirement Investment Accounts: Include stocks, bonds, or mutual funds outside retirement plans.

- Existing Life Insurance Policies: Account for death benefits from current policies.

- Dedicated College Funds: Include savings earmarked for education, such as 529 plans.

Step 3: Calculate Your Coverage Need – Subtract your total liquid assets from your total financial obligations to identify the shortfall. This amount provides a preliminary estimate of the life insurance coverage required to ensure your family’s financial stability after your passing.

For example, if your financial obligations total $500,000 and your liquid assets amount to $150,000, your estimated coverage need would be $350,000 ($500,000 – $150,000). However, this figure should be further adjusted based on your specific circumstances and long-term goals.

↳ 10 × Income

The 10× Income method is recognized as one of the simplest and most efficient approaches to estimating your life insurance coverage needs, providing a quick benchmark by multiplying your current annual income by ten. The formula is straightforward:

- Coverage Needed = 10 × Current Income

This method assumes that replacing approximately ten years of income will sufficiently support your dependents, making it a convenient option for those seeking a rapid initial estimate. However, its simplicity introduces notable limitations, as it does not account for a comprehensive view of your financial profile, including debts, assets, and specific family requirements, which could result in an inaccurate assessment if used as the sole determinant.

Example: If your annual salary is $100,000, multiplying it by 10 yields an estimated coverage amount of $1 million. Nevertheless, this figure should be refined through a more thorough analysis to align with your specific financial circumstances and ensure optimal protection for your loved ones.

↳ Dime Formula

The DIME Formula provides a structured methodology for evaluating your life insurance coverage needs by analyzing four critical categories—Debt, Income, Mortgage, and Education—represented by the acronym DIME. This approach offers a comprehensive framework to ensure your policy aligns with your financial responsibilities. Here’s how it operates:

- Debt – Compile all outstanding debts, including credit card balances, car loans, and personal loans, to ensure these liabilities are addressed and do not become a burden on your loved ones.

- Income – Assess the number of years your family will need financial support following your passing, then multiply your annual income by that duration to calculate the income replacement required for their stability (e.g., $75,000 × 10 years = $750,000).

- Mortgage – Determine the remaining balance of your mortgage, if applicable, to provide funds for its payoff, thereby securing your family’s housing stability.

- Education – Estimate the costs of your children’s college education, if relevant (e.g., $50,000 per child), to prepare for future educational expenses.

By summing these obligations, you obtain a preliminary estimate of your coverage needs, establishing a robust foundation for planning. However, this formula has a significant limitation: it does not consider your current liquid assets—such as savings, investments, or existing insurance policies—which may lead to an overestimation of the required coverage.

↳ Income Replacement

The Income Replacement method aims to secure sufficient life insurance coverage to fully replace your income, enabling your beneficiaries to maintain their standard of living without depleting the principal payout for daily expenses. This approach ensures the funds remain preserved for future financial goals.

It assumes that your beneficiaries will invest the lump-sum death benefit and use the resulting returns to cover ongoing expenses—such as household costs or childcare—while keeping the principal intact. As income needs decrease, such as when children gain independence, the principal can then be utilized for significant expenses like college tuition or retirement planning. The formula for this method is:

- Coverage Needed = Current Income ÷ Assumed Rate of Return

For stay-at-home parents – Instead of using current income, you estimate the annual cost to hire someone to perform their essential duties, such as childcare, household management, or other responsibilities, ensuring these contributions are adequately accounted for in the coverage plan.

Example: If your annual income is $200,000 and you assume a 6% rate of return, divide $200,000 by 0.06, yielding a coverage amount of approximately $3.33 million. If your beneficiary receives this $3.33 million payout and invests it in a diversified portfolio generating 6% annually, the resulting $200,000 in yearly returns can replace your income, ensuring financial stability while preserving the principal for future needs.

↳ Online Calculators

Online calculators provide a convenient and user-friendly means to estimate your life insurance coverage needs, offering a broad overview with minimal effort. While they serve as a valuable starting point for assessing your requirements, it’s essential to examine the methodology behind each tool, as variations in assumptions and calculations can significantly impact the accuracy of the estimate.

Below, we’ve curated a list of reputable online calculators for your consideration. Since these are external resources, we strongly recommend reviewing their methodology and terms of use to ensure their approach aligns with your financial planning goals.

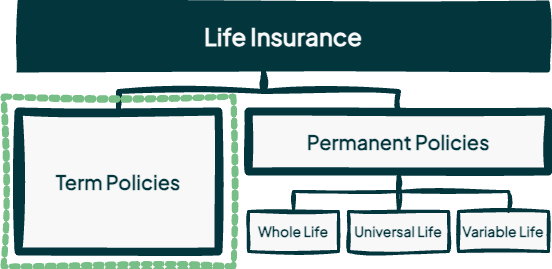

Term Policy

A term life insurance policy is one of the two primary categories of life insurance, the other being permanent life insurance. This policy type provides financial protection for a defined period, known as the term, by delivering a death benefit to the designated beneficiary if the insured passes away during that time frame. Unlike permanent life insurance, term life insurance excludes an investment or savings component, positioning it as a simple and cost-effective solution for temporary coverage needs.

A term life insurance policy is one of the two primary categories of life insurance, the other being permanent life insurance. This policy type provides financial protection for a defined period, known as the term, by delivering a death benefit to the designated beneficiary if the insured passes away during that time frame. Unlike permanent life insurance, term life insurance excludes an investment or savings component, positioning it as a simple and cost-effective solution for temporary coverage needs.

For instance, if you acquire a 20-year term life insurance policy and pass away within those 20 years, your beneficiary will receive the predetermined death benefit, provided premiums are paid promptly to keep the policy active. Should you outlive the term, the policy expires, premium payments cease, and no death benefit is payable. Consequently, if you pass away after the term concludes, no benefits are available unless the policy was renewed or converted prior to its expiration.

Term lengths generally range from 1 to 30 years, with the most common durations being 10, 20, or 30 years, depending on the insurer and the policyholder’s specific needs. Some policies offer renewable terms, allowing the policyholder to extend coverage without additional medical underwriting, although premiums may rise with age to reflect increased risk. Additionally, certain term policies include a convertibility option, enabling the policyholder to transition to a permanent policy within a designated timeframe, regardless of changes in health status.

Compared to permanent life insurance, term life insurance typically features lower premiums, making it an appealing option for individuals seeking affordable coverage for specific financial obligations, such as mortgage repayment, funding a child’s education, or replacing income during working years. However, because term policies do not accumulate cash value, they are strictly protection-oriented and offer no financial return if the insured survives the term.

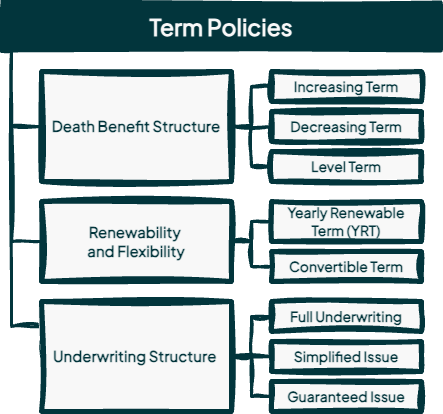

Types of Term Policies

Term life insurance offers a range of policy variations, each with distinct features and cost structures tailored to meet diverse financial needs and long-term goals. However, fundamentally, every term policy variation operates on a core principle: it provides a death benefit for a set period, with coverage ending at the term’s conclusion unless options such as renewal or conversion are exercised, as outlined in the policy’s terms.

Term life insurance offers a range of policy variations, each with distinct features and cost structures tailored to meet diverse financial needs and long-term goals. However, fundamentally, every term policy variation operates on a core principle: it provides a death benefit for a set period, with coverage ending at the term’s conclusion unless options such as renewal or conversion are exercised, as outlined in the policy’s terms.

This diversity ensures that whether you’re addressing short-term financial obligations or seeking extended security for your family, there’s a term policy suited to your circumstances. Ultimately, the most suitable policy hinges on your individual financial situation, lifestyle factors, and long-term aspirations, underscoring the importance of carefully evaluating your needs before making a selection.

Death Benefit Structure

The death benefit structure of term life insurance determines how the payout to beneficiaries evolves over the policy’s term, offering options designed to address diverse financial planning needs. These variations, tabbed below, include policies with a constant level death benefit, as well as those where the benefit decreases or increases over time, providing flexibility to align coverage with evolving liabilities or financial goals. Comprehending these differences is crucial for selecting a policy that aligns with your specific circumstances and long-term objectives.

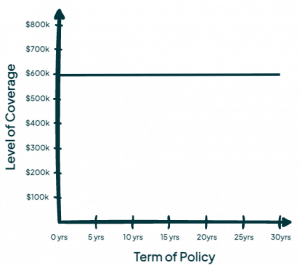

↳ Level Term – Level term life insurance is a straightforward term policy that has a fixed premium and a consistent death benefit over a specified term, typically lasting 10, 20, or 30 years. The term “level” highlights the stable nature of both the premium and death benefit, ensuring reliable coverage throughout the policy duration.

↳ Level Term – Level term life insurance is a straightforward term policy that has a fixed premium and a consistent death benefit over a specified term, typically lasting 10, 20, or 30 years. The term “level” highlights the stable nature of both the premium and death benefit, ensuring reliable coverage throughout the policy duration.

This predictability simplifies budgeting, as premiums remain constant regardless of age or health changes, making it one of the most cost-effective life insurance options—particularly for young, healthy individuals. Overall, level term life policies deliver a simple and accessible solution for securing financial protection during critical life stages.

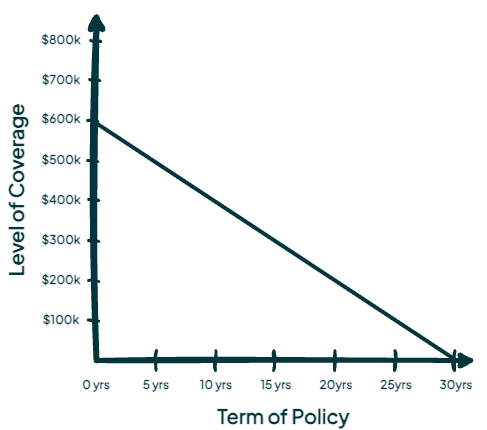

↳ Decreasing Term – Decreasing term life insurance is a specialized policy designed to deliver a death benefit that gradually diminishes over the specified term, typically aligned with declining financial obligations such as a mortgage or loan balance. Premiums may remain level or adjust throughout the term, depending on the policy’s design.

↳ Decreasing Term – Decreasing term life insurance is a specialized policy designed to deliver a death benefit that gradually diminishes over the specified term, typically aligned with declining financial obligations such as a mortgage or loan balance. Premiums may remain level or adjust throughout the term, depending on the policy’s design.

This variation provides a cost-effective solution with reducing coverage, making it an attractive option for individuals seeking protection during specific, diminishing liabilities. It ensures the death benefit corresponds to the remaining debt or financial need at any given time, offering peace of mind.

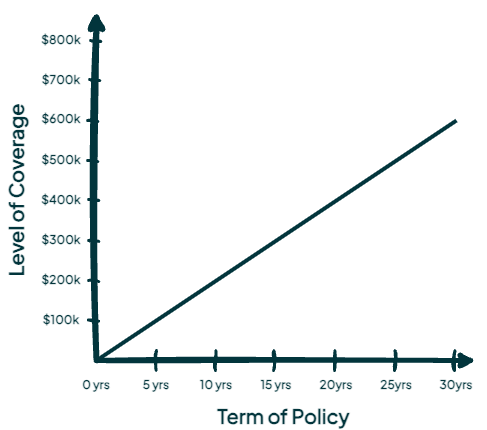

↳ Increasing Term – Increasing term life insurance is a specialized policy designed to provide a death benefit that escalates over the specified term, often aligned with inflation or growing financial responsibilities, such as future education costs or rising income replacement needs. The death benefit typically increases periodically—either annually or at predetermined intervals—while premiums may remain level or adjust according to the policy terms, offering a flexible approach for those anticipating escalating financial obligations.

↳ Increasing Term – Increasing term life insurance is a specialized policy designed to provide a death benefit that escalates over the specified term, often aligned with inflation or growing financial responsibilities, such as future education costs or rising income replacement needs. The death benefit typically increases periodically—either annually or at predetermined intervals—while premiums may remain level or adjust according to the policy terms, offering a flexible approach for those anticipating escalating financial obligations.

This structure ensures coverage adapts to evolving economic conditions or personal circumstances, positioning it as a strategic option for individuals planning for long-term financial security.

Renewability & Flexibility

Term life insurance offers “renewability and flexibility” features that allow policies to adapt to your evolving life circumstances, ensuring coverage remains effective or adjustable to meet changing needs over time. Whether through extending protection via renewals or accessing options like conversion, these policy variations enable you to protect your loved ones without the burden of reapplication or requalification across key life milestones. Tabbed below are the specific options that provide this adaptability.

↳ Yearly Renewable Term (YRT) – Yearly Renewable Term (YRT) life insurance is a flexible policy offering coverage for a one-year term, with the option to renew annually without requiring new medical underwriting. This feature makes it an accessible choice for individuals anticipating changes in their health or circumstances over time. While renewability ensures continued protection, premiums rise each year based on the insured’s advancing age, reflecting the increased risk to the insurer.

This policy is particularly well-suited for those needing temporary coverage during transitional phases, such as launching a business or managing short-term debts, while retaining the flexibility to adjust coverage as circumstances evolve.

↳ Convertible Term – Convertible term life insurance is a policy structured to provide coverage for a specified term while offering the distinct option to convert into a permanent life insurance policy without requiring new medical underwriting. This adaptability enables policyholders to address evolving needs—such as securing lifelong protection as health conditions change or financial responsibilities grow—without the need for requalification. Typically, the conversion must take place within a designated timeframe or before a specified age, as stipulated by the policy terms.

Underwriting Structure

The underwriting structure of term life insurance provides a range of pathways, enabling coverage options that cater to a diverse array of health profiles and personal circumstances. Underwriting is the insurer’s process for evaluating risk and determining eligibility, ensuring that each policyholder receives protection tailored. Tabbed below details these various underwriting structures for a term policy.

↳ Full Underwriting – Full underwriting term life insurance entails a thorough risk assessment process that involves a detailed medical examination, a comprehensive health history review, and often additional lifestyle information to determine eligibility and set premiums. This method ensures coverage is precisely tailored to the insured’s risk profile.

Commonly applied to policies with varied death benefit structures—such as level term, decreasing term, and increasing term—this approach enables insurers to offer competitive rates to individuals in good health, typically over terms of 10, 20, or 30 years, making it an ideal choice for those seeking long-term financial protection. By leveraging in-depth health evaluations, full underwriting provides robust coverage that aligns closely with the insured’s specific needs and circumstances.

↳ Simplified Issue – Simplified issue term life insurance streamlines the underwriting process by requiring only a few health-related questions instead of a full medical examination, providing a convenient and efficient pathway to coverage for individuals seeking a less invasive application process. This method reduces the need for extensive health documentation, facilitating faster policy issuance—often within days—making it an ideal option for those with minor health concerns or those prioritizing speed and simplicity in securing protection over a specified term.

While premiums may be higher than those of fully underwritten policies due to the limited risk assessment, simplified issue policies offer accessible death benefit protection, ensuring financial security for beneficiaries.

↳ Guaranteed Issue – Guaranteed issue term life insurance removes the requirement for medical examinations or health questions, providing a fully accessible underwriting process that ensures coverage for individuals who might otherwise be declined due to pre-existing conditions, advanced age, or other risk factors.

This approach emphasizes inclusivity, offering immediate protection over a specified term—often with smaller death benefit amounts designed for final expenses or limited financial needs—while typically entailing higher premiums to account for the insurer’s elevated risk.

Ideal for those seeking a streamlined application process, guaranteed issue policies provide straightforward death benefit protection, enabling hard-to-insure applicants to achieve financial peace of mind for their beneficiaries.

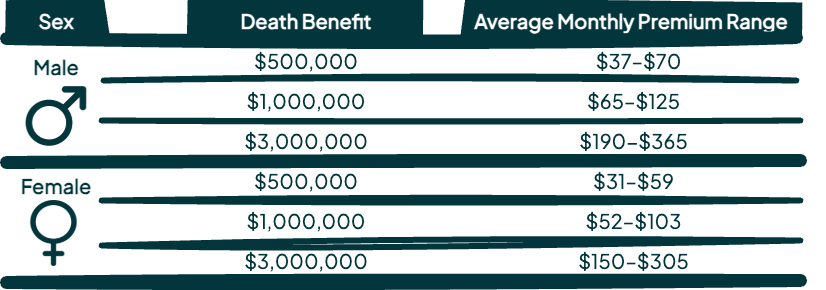

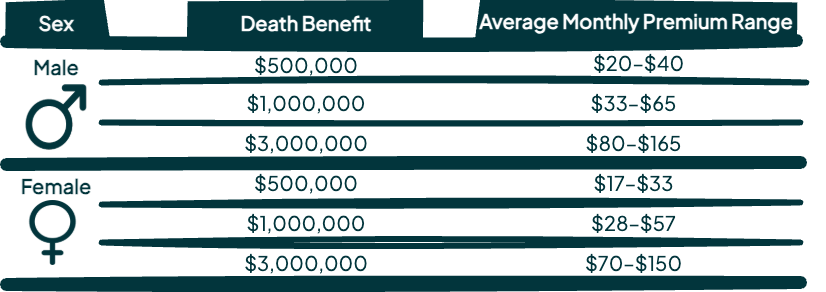

Average Premium Cost

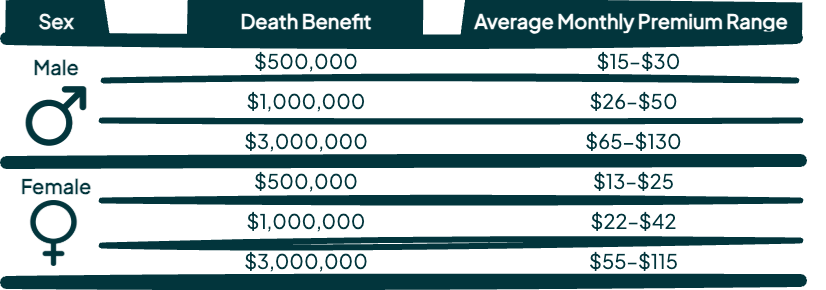

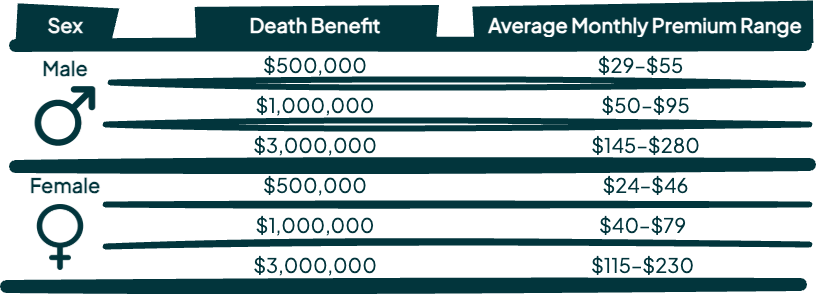

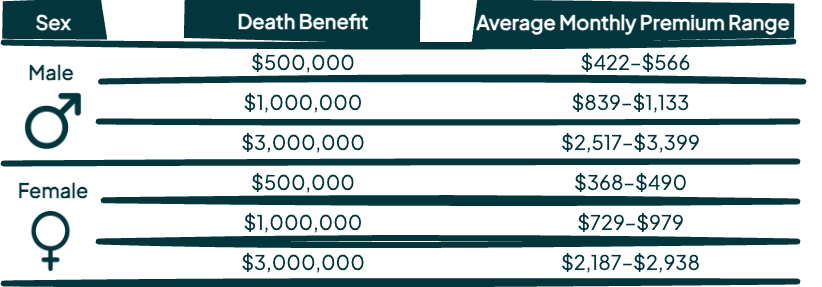

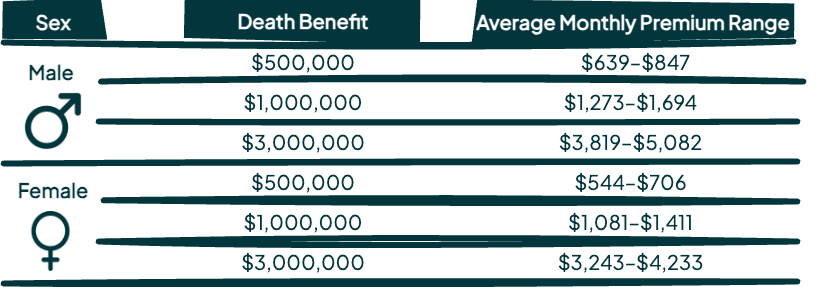

The premium cost of term life insurance is influenced by factors such as term duration, coverage level, age, gender, and personal health. Tabbed below are average premium cost ranges, providing insight into cost variations to help you assess affordability and plan effectively. Understanding the balance between price and protection enables informed decisions tailored to your budget. For more precise figures, consider using online comparison tools or requesting quotes directly from top-tier insurers to better navigate the market.

↳ Age 30, Healthy Non-smoker

These are premium estimate ranges for a healthy, non-smoking individual. Rates are based on 2025 data from sources like Policygenius, ValuePenguin, and NerdWallet, with estimates for $3,000,000 coverage due to limited direct data. Actual rates may vary by insurer, state, and specific health details, so the average ranges can differ significantly.

↳ Age 40, Healthy Non-smoker

These are premium estimate ranges for a healthy, non-smoking individual. Rates are based on 2025 data from sources like Policygenius, ValuePenguin, and NerdWallet, with estimates for $3,000,000 coverage due to limited direct data. Actual rates may vary by insurer, state, and specific health details, so the average ranges can differ significantly.

Personalized Quotes

Obtaining multiple personalized quotes and comparing policy types, features, and costs is a strategic approach to understanding the term life insurance market and its pricing dynamics. Tabbed below is a curated selection of comparison tools and direct insurers to help you access tailored quotes efficiently, empowering you to make well-informed decisions about your coverage. By exploring these options and evaluating the associated cost trade-offs, you can confidently choose a policy that aligns with your financial needs and long-term goals, ensuring both affordability and optimal protection for your loved ones.

↳ Comparison Tools

These websites streamline the process of finding affordable term life insurance by aggregating quotes from multiple insurers, saving time and ensuring competitive rates.

↳ Top Insures (direct quotes)

The goal was to identify top term insurers that balance low costs with high reliability, considering factors such as premium rates, financial strength (AM Best ratings), customer satisfaction (J.D. Power scores, NAIC complaint indices), and policy features (e.g., coverage limits, term lengths, conversion options).

Permanent Policy

A permanent life insurance policy is one of the two primary categories of life insurance, alongside term life insurance. Unlike term life insurance, which provides coverage for a specified duration (e.g., 10, 20, or 30 years) and expires if the insured outlives the term, permanent life insurance is structured to provide protection for the insured’s entire lifetime, as long as premiums are paid as required. This lifelong coverage guarantees a death benefit to designated beneficiaries upon the insured’s passing, making it a vital tool for long-term financial strategies, such as estate planning, wealth transfer, or ensuring lasting financial security for loved ones.

A permanent life insurance policy is one of the two primary categories of life insurance, alongside term life insurance. Unlike term life insurance, which provides coverage for a specified duration (e.g., 10, 20, or 30 years) and expires if the insured outlives the term, permanent life insurance is structured to provide protection for the insured’s entire lifetime, as long as premiums are paid as required. This lifelong coverage guarantees a death benefit to designated beneficiaries upon the insured’s passing, making it a vital tool for long-term financial strategies, such as estate planning, wealth transfer, or ensuring lasting financial security for loved ones.

Beyond the death benefit, permanent life insurance policies feature a cash value component, a distinguishing element that accumulates over time, often on a tax-deferred basis. This cash value acts as a savings or investment vehicle within the policy, growing through mechanisms specific to each policy type (e.g., guaranteed interest, market-linked returns, or investment performance). Policyholders can access this cash value during their lifetime through withdrawals or policy loans, providing flexibility to address financial needs. However, loans accrue interest, and withdrawals or unpaid loans may reduce both the cash value and the death benefit, requiring careful management to preserve the policy’s benefits.

Due to the inclusion of a savings component, the assurance of lifelong coverage, and the associated administrative and investment costs, premiums for permanent life insurance are generally higher than those for term life insurance, reflecting its dual role as both a protective measure and a financial asset.

Types of Permanent Policies

Permanent life insurance encompasses three primary types: (1) whole life, (2) universal life, and (3) variable life, each with distinct features tailored to diverse financial needs and risk profiles. All share the fundamental benefit of permanent insurance—lifelong coverage for the insured, provided premiums are paid as required—guaranteeing a death benefit for beneficiaries upon the insured’s passing. The differences among them lie in premium payment structures, death benefit adjustability, and cash value growth mechanisms.

Permanent life insurance encompasses three primary types: (1) whole life, (2) universal life, and (3) variable life, each with distinct features tailored to diverse financial needs and risk profiles. All share the fundamental benefit of permanent insurance—lifelong coverage for the insured, provided premiums are paid as required—guaranteeing a death benefit for beneficiaries upon the insured’s passing. The differences among them lie in premium payment structures, death benefit adjustability, and cash value growth mechanisms.

Whole life offers stability through fixed premiums and guaranteed cash value growth, universal life provides flexibility with adjustable premiums and varied cash value growth options, and variable life emphasizes investment-driven cash-value growth within a fixed premium framework.

Whether you prioritize predictability, adaptability, or the potential for higher returns through investments, these options enable you to choose a policy that aligns with your financial goals, risk tolerance, and long-term objectives. Additionally, the type selected influences how the cash value can be utilized—such as offsetting premiums in universal life or supporting investment strategies in variable life—enhancing the policy’s overall utility.

Table Summary - Whole vs. Universal vs. Variable Life

| Feature | Whole Life | Universal Life | Variable Life |

|---|---|---|---|

| Coverage |

|

|

|

| Premiums | Fixed, predictable |

|

Fixed, consistent |

| Cash Value Growth |

|

|

|

| Cash Value Use |

|

|

|

| Risk Level | Low, stable growth |

|

|

| Flexibility | Low, fixed terms |

|

|

Types of Permanent Life Insurance

(1) Whole Life

Whole life insurance is a foundational type of permanent life insurance, emphasizing stability, predictability, and lifelong protection. This policy type integrates a guaranteed death benefit with a guaranteed cash value component that accumulates over time, making it an excellent option for individuals seeking both enduring coverage and a reliable savings mechanism. The death benefit is assured for the insured’s entire lifetime, as long as premiums are paid as required, and remains unaffected by market volatility, health changes, or economic conditions.

Whole life insurance is a foundational type of permanent life insurance, emphasizing stability, predictability, and lifelong protection. This policy type integrates a guaranteed death benefit with a guaranteed cash value component that accumulates over time, making it an excellent option for individuals seeking both enduring coverage and a reliable savings mechanism. The death benefit is assured for the insured’s entire lifetime, as long as premiums are paid as required, and remains unaffected by market volatility, health changes, or economic conditions.

Premiums for whole life insurance are set at the policy’s outset and remain fixed throughout its duration, providing predictable budgeting in contrast to the adjustable payment structures of universal or variable life policies. The cash value grows at a guaranteed rate, typically tied to a conservative interest rate (e.g., 2–4%, depending on the insurer), ensuring steady, low-risk growth. Upon the insured’s passing, the cash value is retained by the insurer to offset the death benefit cost and is not paid separately to beneficiaries, though it supports the policy’s sustainability during the insured’s lifetime.

Lifelong Coverage

- Guarantees coverage for the insured’s entire life, provided premiums are paid as agreed.

- Ensures beneficiaries receive a death benefit, regardless of the timing of the insured’s passing.

Fixed Premium

Guaranteed Death Benefit

Cash Value (Guaranteed Rate)

- Includes a cash value component that grows over time on a tax-deferred basis.

- Acts as a savings or investment element within the policy, with growth guaranteed by the insurer at a conservative rate.

- Policyholders can access this cash value for various needs, though it is retained by the insurer upon death to support the death benefit payout.

Loans & Withdraws

Surrender Options

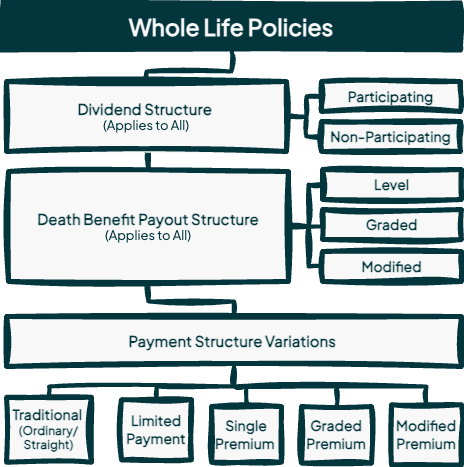

Dividend Structure

When selecting a whole life insurance policy, the insurer classifies it as either participating or non-participating, a designation based on its dividend structure. This classification significantly impacts the policy’s overall value and flexibility, making it a critical factor for prospective policyholders to consider. The dividend structure often reflects the insurer’s organizational framework: mutual insurance companies (owned by policyholders) typically issue participating policies while stock insurance companies (owned by shareholders) often opt for non-participating policies. Tabbed below details the two dividend structures.

↳ Participating – Participating whole life policies enable policyholders to potentially receive dividends, which are a share of the insurer’s surplus profits from investment returns, operational efficiencies, or favorable mortality and claims experience. Although dividends are not guaranteed, they offer strategic options that enhance the policy’s flexibility and long-term value. Policyholders can:

- Reduce Future Premiums: Use dividends to offset out-of-pocket premium costs, improving affordability over time.

- Purchase Paid-Up Additions: Apply dividends to acquire additional coverage without further underwriting, boosting both the death benefit and cash value.

- Receive Cash Disbursement: Opt for dividends as a direct cash payment, providing immediate liquidity for needs like emergency expenses or supplemental income.

The availability and amount of dividends depend on the insurer’s financial performance, introducing variability that policyholders must consider. Dividends are typically declared annually and may vary with economic conditions, investment yields, or claims experience, necessitating a long-term perspective to maximize their benefits.

↳ Non-participating – Non-participating policies do not offer dividends, providing fixed benefits—including premiums, death benefit, and cash value growth—unaffected by the insurer’s profitability or market fluctuations. This structure ensures complete predictability, appealing to those who prioritize certainty in their financial planning.

As a result, non-participating whole life policies often have lower initial premiums, making them a cost-effective choice for individuals who value affordability and a straightforward financial commitment over the potential for dividend-driven growth. However, the absence of dividends limits the policy’s adaptability to evolving financial needs or the ability to benefit from insurer profitability.

Death Benefit Payout Structure

The death benefit payout structure is a critical component of whole life insurance, governing how the death benefit is disbursed to beneficiaries during the initial premium phase, directly influencing the policy’s cost, coverage, and suitability for individual needs. Whole life policies have three primary death benefit payout structures—level, graded, and modified—each designed to balance immediate coverage with affordability and risk management. These three options determine if the death benefit is guaranteed protection from the outset or has deferred full benefits, making it essential to understand their mechanics and implications for effective planning.

↳ Level Death Benefit – The level death benefit is the core payout option in whole life insurance, providing immediate and consistent coverage from the policy’s inception, ensuring a guaranteed death benefit for beneficiaries upon the insured’s passing. The full death benefit, fixed at the policy’s outset, is available from day one, subject to a standard exclusion for suicide within the first two years, during which only premiums paid are typically refunded.

Individuals in good health, often classified as Preferred or Standard risk categories, qualify more easily due to their lower mortality risk, supporting the insurer’s commitment to an immediate payout. However, those with pre-existing conditions, advanced age (e.g., over 70), or substandard health may face restrictions and could be directed to graded or modified death benefit options with deferred full coverage.

↳ Graded Death Benefit – The graded death benefit offers provides partial coverage in the initial years before transitioning to full benefits after a specified period. This structure is designed to gradually increase the death benefit over the initial period (e.g., 2–3 years), starting with a partial payout (premiums plus interest) and transitioning to the full benefit. The partial payout is intended as a stepped benefit, often structured to increase each year during the graded period (e.g., 30% of the death benefit in Year 1, 60% in Year 2, 100% in Year 3), though some policies may simplify this to premiums plus interest for non-accidental deaths.

This option is often for individuals with moderate health risks, such as those with manageable pre-existing conditions (e.g., controlled diabetes), who may not qualify for immediate full coverage. However, the limited early protection may leave beneficiaries financially vulnerable during the graded period.

↳ Modified Death Benefit – The modified death benefit provides limited coverage during an initial waiting period before transitioning to full benefits, tailored for those with specific health or financial considerations. This structure imposes a strict waiting period with no partial death benefit beyond a refund of premiums plus interest during the initial 2–3 years. It’s not designed to gradually increase coverage but to delay full coverage entirely, focusing on affordability for high-risk individuals. The early payout is strictly a refund mechanism, not a stepped benefit, meaning there’s no progression toward the full death benefit until the waiting period ends.

This structure is ideal for individuals with pre-existing conditions, advanced age, or substandard health who may not qualify for immediate full coverage, as well as those seeking affordable final expense protection. However, the absence of a partial benefit during the waiting period can leave beneficiaries with limited protection beyond premium refund

Payment Structure Variations

Whole life insurance policies provide a range of payment structures tailored to diverse financial needs and goals, enabling policyholders to customize their premium payments while ensuring lifelong coverage. These variations impact the policy’s affordability, the rate of cash value growth, and overall flexibility.

Whether you value predictability, early payment completion, budget-friendly initial costs, or the tax-advantaged growth potential of a single payment, understanding these options ensures they align with your financial circumstances and objectives. Each structure, tabbed below, preserves the core benefits of whole life—guaranteed death benefit and consistent cash value accumulation—while offering distinct approaches to fulfilling premium obligations.

↳ Traditional (Ordinary/Straight) – Traditional whole life insurance, commonly known as ordinary or straight whole life, serves as the foundational form of whole life coverage. It offers lifelong protection with a fixed, level premium payable throughout the insured’s lifetime. The death benefit is guaranteed and remains constant, unaffected by market volatility or health changes, while the cash value accumulates at a steady, guaranteed rate (typically 2–4%, as determined by the insurer).

This structure provides simplicity and predictability, making it an ideal choice for individuals seeking stability and long-term financial security, such as those focused on legacy planning. The consistent premium supports a balanced growth of cash value, which can be accessed through loans or withdrawals, though it is retained by the insurer to offset the death benefit upon the insured’s passing.

↳ Limited Payment – The limited payment structure allows policyholders to pay higher premiums over a specified period—typically 10, 20, or 30 years—after which the policy becomes fully paid up, with coverage continuing for life without further premium obligations. Both the death benefit and cash value growth are guaranteed, consistent with traditional whole life, though the accelerated payment schedule promotes faster cash value accumulation due to the front-loaded premiums.

This variation is well-suited for individuals aiming to complete premium payments during their working years, such as professionals with stable early-career income, ensuring lifelong protection and a substantial cash value without ongoing financial commitments. The higher initial premiums reflect the condensed payment timeline but enhance the policy’s value as a savings tool over time.

Types of Permanent Life Insurance

(2) Universal Life

Universal life insurance, a type of permanent life insurance, is characterized by its flexibility in premium payments and death benefits, distinguishing it from the rigid structure of whole life insurance. Unlike whole life, which features fixed premiums and benefits, universal life allows policyholders to adjust both premiums and the death benefit within defined limits, providing a customizable approach to lifelong coverage.

Universal life insurance, a type of permanent life insurance, is characterized by its flexibility in premium payments and death benefits, distinguishing it from the rigid structure of whole life insurance. Unlike whole life, which features fixed premiums and benefits, universal life allows policyholders to adjust both premiums and the death benefit within defined limits, providing a customizable approach to lifelong coverage.

This flexibility is paired with a cash value component that accumulates over time, typically on a tax-deferred basis, serving as a savings or investment element accessible through loans or withdrawals (subject to policy terms). Universal life is well-suited for those seeking a balance between protection and financial adaptability, making it an effective tool for estate planning, income supplementation, or adjusting to changing economic circumstances.

The cash value grows based on an interest rate credited by the insurer, often including a guaranteed minimum rate (e.g., 2–3%) to ensure growth even in adverse market conditions. Variations may tie cash value growth to a market index or investment sub-account, balancing growth potential with security to cater to diverse risk tolerances while preserving the policy’s core flexibility.

Universal life policies typically offer two death benefit options—level and increasing—offering further customization. The level option provides a fixed payout, while the increasing option allows the death benefit to grow alongside the cash value, subject to insurer approval for adjustments. This dual structure, combined with flexible premiums, sets universal life apart from other permanent policies, though it requires careful management to prevent policy lapse due to insufficient funding.

Lifelong Coverage

- Guarantees coverage for the insured’s lifetime, provided the policy remains adequately funded through premium payments.

- Requires diligent monitoring of the policy’s funding level—particularly the cash value’s ability to cover costs—to prevent lapse, especially as insurance costs rise with age.

Flexible Premium

Adjustable, Guaranteed Death Benefit

Cash Value (Guaranteed, Index-linked or Investment Sub-Acccount)

- Includes a cash value component that grows over time on a tax-deferred basis, acting as a savings or investment element within the policy.

- Growth can be guaranteed by the insurer at a minimum rate (e.g., 2–3%), with variations linking growth to market indices or investment sub-accounts, offering a balance of security and potential returns.

Loans & Withdraws

Surrender Options

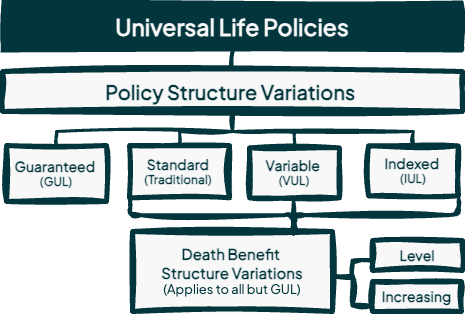

Policy Structure Variations

Universal life insurance includes a variety of policy structures, each designed to address distinct financial priorities and risk profiles while maintaining the core benefits of lifelong coverage and flexible premiums. These variations tabbed below—Traditional Universal Life, Indexed Universal Life (IUL), Variable Universal Life (VUL), and Guaranteed Universal Life (GUL)—differ primarily in their cash value growth mechanisms and the balance between guaranteed returns and investment potential. This diversity enables policyholders to choose a structure that aligns with their goals, whether they prioritize steady growth, market-linked returns, investment flexibility, or assured coverage with minimal cash value accumulation.

↳ Standard / Traditional – Traditional universal life insurance, often regarded as the foundational form of universal life policies, provides a balanced approach by offering lifelong coverage within a flexible yet predictable framework. It ensures a guaranteed death benefit for the insured’s entire lifetime, provided premiums are paid as required, while allowing adjustable premium and death benefit options.

Policyholders can modify their premium payments within policy limits—increasing or decreasing contributions as their financial circumstances change—provided the cash value covers the cost of insurance and administrative fees. Likewise, the death benefit can be adjusted, with increases requiring additional underwriting and decreases permitted to align with evolving needs.

This policy type includes a cash value component that grows based on a guaranteed interest rate credited by the insurer. The rate may vary within a range determined by the insurer, reflecting current market conditions, but a minimum guaranteed rate ensures baseline growth even in low-interest environments. This combination makes it an attractive option for those seeking a blend of stability and adaptability.

↳ Indexed (IUL) – Indexed universal life (IUL) insurance, a variation of universal life insurance, combines the flexibility of adjustable premiums and death benefits with the potential for enhanced cash value growth linked to market performance. It provides lifelong coverage for the insured, provided premiums are paid as required, while utilizing the performance of a market index, such as the S&P 500, to drive cash value accumulation.

Designed for individuals seeking a balance between growth potential and downside protection, IUL offers higher return possibilities compared to traditional universal life, moderated by safeguards against market losses, making it an appealing choice for those comfortable with moderate risk.

The cash value in an IUL policy grows based on the performance of a chosen index, with the insurer crediting interest up to a predetermined cap (e.g., 10–12% annually) while ensuring a floor (e.g., 0–1%) to prevent losses in declining markets. This structure enables policyholders to capitalize on market upswings while minimizing risk, though the capped returns limit the upside compared to direct market investments.

Premiums and death benefits remain adjustable within policy limits, allowing modifications to align with evolving financial needs. The policy also offers two death benefit options: a level death benefit, which maintains a fixed payout, or an increasing death benefit, which grows alongside the cash value, providing customizable protection.

↳ Variable (VUL) – Variable universal life (VUL) insurance combines the flexibility of universal life with investment opportunities, appealing to policyholders with a higher risk tolerance and a desire for potential market-driven returns. Like other universal life policies, VUL ensures lifelong coverage for the insured, provided premium payments are maintained sufficiently, while offering adjustable premiums and death benefits to adapt to changing financial needs.

What distinguishes VUL is its cash value component, which is directly tied to investment options selected by the policyholder—such as stocks, bonds, or mutual funds—offering the potential for significant growth but also exposing the policy to market volatility. The cash value grows or declines based on the performance of these chosen investments, with no guaranteed minimum rate, unlike traditional or indexed universal life policies.

This market-driven approach allows for higher returns compared to the more conservative growth of other universal life variants, but it also carries the risk of loss if investments underperform. Policyholders can allocate their cash value across various sub-accounts provided by the insurer, tailoring their investment strategy to align with their financial goals.

The death benefit can be structured as a level amount, which remains constant, or as an increasing amount that grows alongside the cash value, offering customization while requiring diligent management to ensure the policy remains adequately funded

↳ Guaranteed (GUL) – Guaranteed universal life (GUL) insurance, a specialized form of universal life insurance, prioritizes lifelong coverage and a guaranteed death benefit, making it an ideal option for individuals focused on financial security over cash value accumulation. Unlike other universal life variants, GUL ensures a death benefit for the insured’s entire lifetime, provided premiums are paid as required, while placing minimal emphasis on investment growth.

This policy appeals to those seeking a cost-effective alternative to whole life insurance, with premiums often lower than those of traditional universal life, though it forgoes the substantial cash value growth potential of indexed or variable options.

The cash value component in a GUL policy is typically minimal or negligible, as the focus remains on securing the death benefit rather than developing a savings element. Premiums are generally fixed or offer limited flexibility. The death benefit is guaranteed and remains constant, lacking the adjustable or increasing options found in other universal life policies. This straightforward approach, combined with its predictable cost, makes GUL a preferred choice for estate planning or supplementing other insurance needs.

Death Benefit Structure Variations

Universal life insurance provides distinct death benefit structures to meet diverse financial planning needs, enabling policyholders to customize their coverage. These variations—level and increasing—offer a fixed payout or one that grows with the policy’s cash value, providing flexibility across most universal life types, including Traditional, Indexed (IUL), and Variable (VUL), while Guaranteed Universal Life (GUL) typically features a fixed benefit. This adaptability allows policyholders to align their death benefit with long-term goals, balancing predictability with potential growth.

↳ Level – The level death benefit option provides a fixed payout throughout the policy’s duration, ensuring a consistent amount for beneficiaries upon the insured’s passing. This structure offers simplicity and predictability, as the death benefit remains unaffected by the policy’s cash value performance, even in variable growth policies such as Indexed (IUL) or Variable Universal Life (VUL).

For instance, if a policyholder selects a $500,000 level death benefit, that amount remains constant regardless of whether the cash value increases or decreases. In this case, the total death benefit paid to beneficiaries is the fixed amount, with any accumulated cash value potentially used to offset the insurer’s costs, depending on the policy’s terms.

The level death benefit suits those prioritizing certainty and a stable legacy for their loved ones, making it particularly appealing in Traditional Universal Life or IUL, where cash value fluctuations do not impact the guaranteed payout.

↳ Increasing – The increasing death benefit option enables the payout to grow over time, linked to the policy’s cash value accumulation, offering a dynamic approach to coverage. Under this structure, the death benefit begins at a base amount and increases as the cash value grows, potentially providing a higher payout to beneficiaries if the policy performs well.

For example, in a Variable Universal Life (VUL) policy with a $500,000 base death benefit and a cash value that rises to $100,000 due to strong investment performance, the total death benefit would be $600,000 (base plus cash value).

This option is available in Traditional Universal Life, Indexed (IUL), and VUL, where cash value growth—driven by interest-based, index-linked, or investment-based mechanisms—can enhance the benefit. However, it demands careful monitoring, as poor cash value performance (e.g., in VUL during market downturns) may limit growth, and increasing the base amount may require additional underwriting.

The increasing death benefit is well-suited for policyholders aiming to maximize their legacy by leveraging the growth potential of their policy’s cash value, though premiums for this option are typically higher than those for a level death benefit policy.

Types of Permanent Life Insurance

(3) Variable Life

Variable life insurance, a type of permanent life insurance, combines lifelong coverage with a cash value component directly tied to investment performance, offering policyholders the potential for significant growth alongside a guaranteed minimum death benefit. Introduced as an alternative to traditional whole life insurance, variable life allows the cash value to be invested in a range of sub-accounts—such as stocks, bonds, or mutual funds—where returns depend on market outcomes.

Unlike universal life insurance, which prioritizes flexible premiums and death benefits, variable life features fixed premiums, establishing a structured payment schedule while incorporating investment risk and reward. This blend of stability and opportunity attracts individuals seeking to build wealth within their life insurance policy, though it requires a higher tolerance for market fluctuations.

The cash value in a variable life policy grows or declines based on the performance of the selected investment options, with no guaranteed minimum return, setting it apart from the interest- or index-based growth of other permanent life products. Policyholders can allocate their premiums across available sub-accounts, customizing their investment strategy to match their risk appetite and financial goals, subject to insurer-imposed restrictions or a default option.

The death benefit is guaranteed at a minimum level, ensuring coverage for the insured’s lifetime as long as premiums are paid, and may increase if the cash value exceeds certain thresholds, depending on the policy design. This structure necessitates active oversight, as poor investment performance can diminish the cash value, potentially jeopardizing the policy’s sustainability over time.

Lifelong Coverage

- Guarantees coverage for the insured’s lifetime, contingent upon consistent payment of fixed premiums.

- The policy’s viability hinges on maintaining adequate cash value to cover costs.

Fixed Premium

Guaranteed Death Benefit

Cash Value (Investment Sub-Accounts)

- Includes a cash value component that grows over time on a tax-deferred basis, serving as a savings or investment element within the policy.

- Accumulates based on the performance of investment sub-accounts chosen by the policyholder, with no guaranteed minimum, exposing it to market risk.

Loans & Withdraws

Surrender Options

Understanding the Cash Value Component

The cash value component is a defining feature of permanent life insurance policies, distinguishing them from term life insurance and providing a dual-purpose mechanism that combines lifelong coverage with a savings or investment element. Found in whole life, universal life, and variable life policies, the cash value accumulates over time on a tax-deferred basis, meaning no taxes are paid on its growth until funds are withdrawn.

While the primary function of permanent life insurance is to provide a death benefit, the cash value serves multiple purposes during the policyholder’s lifetime, including supporting policy costs, offering access to funds, and potentially enhancing the death benefit, depending on the policy structure. Understanding its role is essential for maximizing the benefits of your permanent life insurance policy and ensuring its long-term sustainability.

What Is the Cash Value Component & Its Growth Mechanisms?

The cash value represents a portion of the premiums paid into a permanent life insurance policy that accumulates over time, distinct from amounts allocated to fund the death benefit and administrative costs. After covering the cost of insurance (which rises with age), fees (e.g., administrative or investment management), and other charges, the remaining premium contributes to the cash value. This accumulation grows on a tax-deferred basis, allowing it to compound without immediate tax liability, enhancing its role as a savings vehicle.

The growth mechanism varies by policy type:

- Whole Life: Grows at a guaranteed rate (e.g., 2–4%) set by the insurer, ensuring low-risk, predictable accumulation.

- Universal Life:

- Traditional: Grows based on a credited interest rate with a guaranteed minimum (e.g., 2–3%).

- Indexed (IUL): Tied to a market index (e.g., S&P 500), with a cap (e.g., 10–12%) and floor (e.g., 0–1%) to balance growth and risk.

- Variable (VUL): Linked to investment sub-accounts (e.g., stocks, bonds), with no guaranteed minimum, exposing it to market volatility.

- Guaranteed (GUL): Features minimal or negligible growth, prioritizing the guaranteed death benefit.

- Variable Life: Driven by investment sub-accounts, with no guaranteed minimum, offering high growth potential but full market risk.

How Does the Cash Value Function During Your Lifetime?

The cash value serves multiple key functions while the policyholder is alive, extending the policy’s utility beyond its death benefit:

- Covering Policy Costs:

- Helps pay the cost of insurance (COI), which increases with age, as well as fees and charges (e.g., investment fees in VUL). In universal life, these costs are deducted from the cash value, especially if premiums are reduced or skipped.

- Example: In a Traditional Universal Life policy, if COI and fees total $1,500 annually and the premium paid is $1,000, the remaining $500 is drawn from the cash value.

- Example: In a Traditional Universal Life policy, if COI and fees total $1,500 annually and the premium paid is $1,000, the remaining $500 is drawn from the cash value.

- Helps pay the cost of insurance (COI), which increases with age, as well as fees and charges (e.g., investment fees in VUL). In universal life, these costs are deducted from the cash value, especially if premiums are reduced or skipped.

- Offsetting Premium Payments:

- Whole Life: Indirectly offsets premiums via policy loans or an automatic premium loan (APL) provision, where the insurer uses cash value for missed payments, or through a reduced paid-up option.

- Universal Life: Flexible premiums allow the cash value to directly cover payments in Traditional, IUL, and VUL; GUL’s minimal cash value limits this capability.

- Variable Life: Fixed premiums permit indirect use via loans or automatic premium loan (APL) provision.

- Example: In a variable life policy with $20,000 cash value, you can take a $2,000 loan to pay the fixed premium, though interest accrues on the loan.

- Example: In a variable life policy with $20,000 cash value, you can take a $2,000 loan to pay the fixed premium, though interest accrues on the loan.

- Providing Access to Funds:

- Enables loans or withdrawals for needs like emergencies or retirement, with loans accruing interest (e.g., 4–8%) and withdrawals permanently reducing the cash value. Both can lower the death benefit if unpaid.

- Example: With a $50,000 cash value in a whole life policy, a $10,000 withdrawal leaves $40,000, potentially reducing a $500,000 death benefit to $490,000.

- Example: With a $50,000 cash value in a whole life policy, a $10,000 withdrawal leaves $40,000, potentially reducing a $500,000 death benefit to $490,000.

- Enables loans or withdrawals for needs like emergencies or retirement, with loans accruing interest (e.g., 4–8%) and withdrawals permanently reducing the cash value. Both can lower the death benefit if unpaid.

- Supporting Policy Sustainability:

- Acts as a buffer to prevent lapse, especially in universal and variable life, where underfunding or poor performance can deplete it. Whole life’s guaranteed growth ensures long-term viability.

- Example: In a variable life policy, if investments decline and the cash value falls to $5,000 while annual deductions are $6,000, the policy may lapse without additional premiums.

- Acts as a buffer to prevent lapse, especially in universal and variable life, where underfunding or poor performance can deplete it. Whole life’s guaranteed growth ensures long-term viability.

What Happens to the Cash Value Upon Death?

The treatment of the cash value upon the insured’s death varies by the policy’s death benefit structure:

- Level Death Benefit (Whole Life, Universal Life [Traditional, IUL, VUL, GUL], Variable Life [Standard]):

- The cash value is retained by the insurer to offset the cost of the death benefit. Beneficiaries receive only the guaranteed amount (e.g., $500,000), not the cash value (e.g., $100,000).

- The cash value is retained by the insurer to offset the cost of the death benefit. Beneficiaries receive only the guaranteed amount (e.g., $500,000), not the cash value (e.g., $100,000).

- Increasing Death Benefit (Universal Life [Traditional, IUL, VUL], Variable Life [if provision applies]):

- The cash value is included in the death benefit. Beneficiaries receive the base amount plus the cash value (e.g., $500,000 + $100,000 = $600,000).

- The cash value is included in the death benefit. Beneficiaries receive the base amount plus the cash value (e.g., $500,000 + $100,000 = $600,000).

- Why This Happens:The cash value supports the policy’s funding. In a level structure, it offsets the insurer’s payout costs, while in an increasing structure, it enhances the benefit to reflect its growth.

In-force Illustration Statements

An in-force policy statement, commonly referred to as an in-force illustration or annual statement, is a report provided by the insurer for an active permanent life insurance policy. It offers a detailed overview of the policy’s financial status, including current values, performance metrics, and future projections based on specific assumptions. This document is crucial for policyholders to track their policy, particularly in permanent life insurance where cash value, premiums, and death benefits may vary (e.g., in universal life and variable life) or require management to prevent lapse.

Key Components of an In-Force Policy Statement

The statement typically includes the following information:

- Current Policy Values:

- Cash Value: The current balance, reflecting accumulated premiums, growth (e.g., interest, index returns, or investment performance), and deductions (e.g., cost of insurance, fees).

- Example: A universal life policy might show $25,000.

- Death Benefit: The current amount, which may be fixed (whole life, GUL) or adjustable (universal life, variable life).

- Example: A variable life policy might list a $500,000 minimum, with potential increases if cash value grows.

- Surrender Value: The amount payable upon surrender, calculated as cash value minus surrender charges and outstanding loans.

- Example: $20,000 after a $5,000 charge.

- Example: $20,000 after a $5,000 charge.

- Cash Value: The current balance, reflecting accumulated premiums, growth (e.g., interest, index returns, or investment performance), and deductions (e.g., cost of insurance, fees).

- Premium and Payment Details:

- Premiums Paid: Total premiums paid and the current schedule.

- Example: $2,000/year for whole life.

- Premium Projections: For universal life, shows planned versus minimum premiums needed to maintain coverage, especially when using cash value to offset payments.

- Outstanding Loans: Any loans with accrued interest.

- Example: A $5,000 loan at 6% interest, adding $300/year.

- Example: A $5,000 loan at 6% interest, adding $300/year.

- Premiums Paid: Total premiums paid and the current schedule.

- Cost Breakdown:

- Cost of Insurance (COI): Annual or monthly charge for coverage, increasing with age.

- Example: $1,200/year in a VUL policy.

- Administrative Fees: Costs for policy management.

- Example: $100/year.

- Other Charges: Investment management fees (e.g., 1% of sub-account value in VUL) or rider costs (e.g., long-term care rider).

- Cost of Insurance (COI): Annual or monthly charge for coverage, increasing with age.

- Cash Value Growth and Performance:

- Growth Rate: The current rate of cash value growth, depending on the policy type:

- Whole life: Guaranteed rate (e.g., 3%).

- Universal life: Credited interest (Traditional), index performance (IUL), or investment returns (VUL).

- Variable life: Sub-account performance (e.g., 5% return on equity funds).

- Historical Performance: Past growth trends, particularly for IUL, VUL, or variable life policies.

- Growth Rate: The current rate of cash value growth, depending on the policy type:

- Future Projections:

- Assumed Growth Rates: Estimates of cash value and death benefit based on assumed rates (e.g., 4% interest for universal life, 6% for variable life).

- Sustainability: Duration the policy can remain in force without additional premiums, factoring in deductions and growth.

- Example: A universal life policy with $30,000 cash value and $2,000/year deductions might last 15 years at 3% growth.

- Worst-Case Scenarios: Projections at guaranteed minimum rates (e.g., 0% for IUL floors) to highlight lapse risks.

- Policy Status and Alerts:

- Lapse Risk: Warnings if cash value cannot cover costs, especially in universal life or variable life with underfunding risks.

- Riders and Benefits: Status of additional features (e.g., waiver of premium rider).

- Dividend History (Whole Life, Participating Policies): Dividends paid and their use (e.g., cash, paid-up additions), if applicable.

Why Is an In-Force Policy Statement Important?

- Monitoring Financial Health: It helps you assess whether your policy is performing as expected, particularly for cash value growth and sustainability.

- Example: A VUL policy, you can see if poor investment performance is depleting the cash value.

- Example: A VUL policy, you can see if poor investment performance is depleting the cash value.

- Preventing Lapse: Highlights if cash value can cover costs in universal life, avoiding unintentional termination.

- Adjusting Strategies: Guides decisions like increasing premiums, reallocating sub-accounts (VUL/variable life), or reducing loans to sustain coverage.

- Understanding Costs: Details fees and charges, aiding evaluation of cost-effectiveness.

How to Obtain an In-Force Policy Statement?

Insurers typically issue annual statements automatically, but policyholders can request an updated in-force illustration anytime through their insurer or agent. Some insurers provide real-time access via online portals.

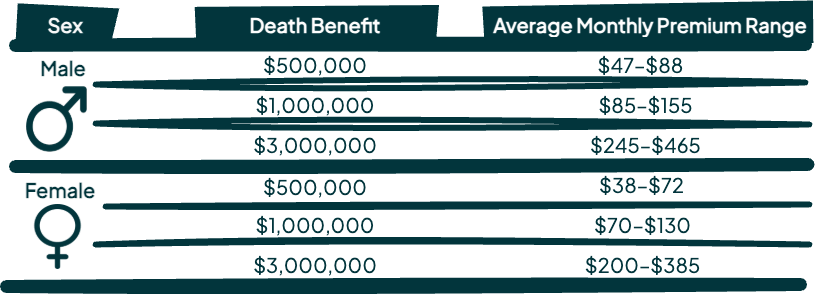

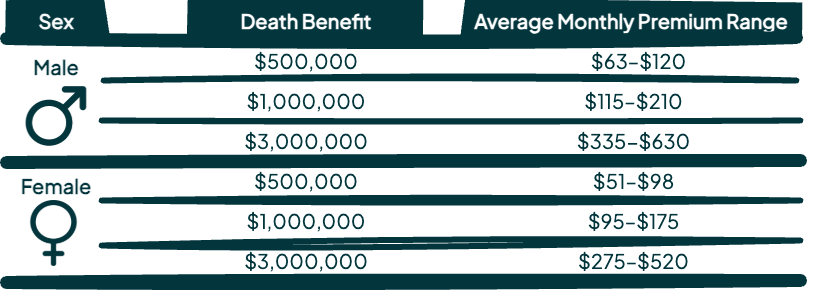

Average Premium Cost

The premium cost of permanent life insurance is influenced by factors such as coverage level, age, gender, and personal health, among others. Tabbed below are average premium cost ranges, providing insight into how these costs vary to help you assess affordability and plan effectively. Understanding the balance between price, protection, and cash value mechanisms enables you to make informed decisions tailored to your budget. For more accurate quotes, consider using online comparison tools or requesting direct quotes from top-tier insurers to better understand market rates.

↳ Whole Life Insurance

These are premium estimate ranges for a healthy, non-smoking individual. Rates are based on 2025 data from sources like Policygenius, ValuePenguin, and NerdWallet, with estimates for $3,000,000 coverage due to limited direct data. Actual rates may vary by insurer, state, and specific health details, so the average ranges can differ significantly.

↳ Universal Life Insurance

Universal life insurance premium costs are typically lower than those of whole life insurance due to the policy’s flexible premium structure and variable cash value growth. These costs can vary widely depending on factors such as insurer practices, health class, policy specifics, and market conditions, making exact averages difficult to determine.

Given this variability, utilizing online comparison tools or requesting direct quotes from top-tier insurers is strongly recommended to ensure the coverage aligns with individual needs.

↳ Variable Life

Variable life insurance premiums typically range between the costs of whole life and universal life, reflecting the policy’s fixed premium structure combined with investment-driven cash value growth. These premiums can vary significantly depending on factors such as insurer pricing, the policyholder’s health class, chosen investment sub-accounts, and market performance, which directly influence the cash value and associated fees.

Given this variability and the impact of investment choices, utilizing online comparison tools or requesting direct quotes from top-tier insurers is advisable to ensure the coverage aligns with individual needs.

Personalized Quotes

Obtaining multiple personalized quotes and comparing policy types, features, and costs is a strategic approach to understanding the permanent life insurance market and its pricing dynamics. Tabbed below is a curated selection of comparison tools and direct insurers to help you access tailored quotes efficiently, enabling you to make well-informed decisions about your coverage. By exploring these options and evaluating the associated cost trade-offs, you can confidently select a policy that aligns with your financial needs and long-term goals, ensuring both affordability and the appropriate level of protection for your loved ones.

↳ Comparison Tools

These websites streamline the process of finding affordable permanent life insurance by aggregating quotes from multiple insurers, saving time and ensuring competitive rates.

↳ Top Insures (direct quote)

The goal is to identify insurers that balance low costs with high reliability, considering factors such as premium rates and financial strength (AM Best ratings).

Riders

A life insurance rider enables policyholders to customize their coverage with tailored enhancements, providing a flexible way to address specific needs without requiring a separate policy. As an optional add-on for both term and permanent policies, riders expand the scope of protection beyond the standard benefits of their respective base policies.

A life insurance rider enables policyholders to customize their coverage with tailored enhancements, providing a flexible way to address specific needs without requiring a separate policy. As an optional add-on for both term and permanent policies, riders expand the scope of protection beyond the standard benefits of their respective base policies.

This customization incurs an additional premium cost, making it essential to assess the financial impact against the potential benefits to ensure a valuable investment. Availability varies by policy and insurer, with some riders subject to eligibility criteria—such as age or health status—and specific terms that may include expiration dates or conditions, requiring careful evaluation to align with your long-term insurance strategy and changing life circumstances.

Accelerated Death Benefit Rider

The accelerated death benefit rider enables policyholders to access a portion of their life insurance death benefit early if diagnosed with a terminal illness, offering critical financial support during a difficult period. Available on both term and permanent policies, this rider allows the insured to use the funds for medical expenses, care costs, or other needs, with the accessed amount reducing the eventual death benefit paid to beneficiaries.

While this rider typically incurs an additional premium, it provides significant peace of mind by ensuring resources are available when most needed. Eligibility generally requires a physician’s certification of a terminal condition, often with a life expectancy of 12 to 24 months, though terms may vary by insurer, making it a valuable option for those seeking flexibility in critical situations.

Critical Illness Rider

The critical illness rider enhances a life insurance policy by providing a lump-sum payment upon diagnosis of a specified serious illness, such as cancer, heart attack, or stroke, delivering financial relief during a period of significant medical and personal challenges. Available for both term and permanent policies, this rider enables the insured to use the payout for treatment costs, living expenses, or other financial needs. Typically, it does not impact the policy’s death benefit, though the rider itself incurs an additional premium.

Eligibility generally requires meeting the insurer’s criteria for covered illnesses, which may vary, making this rider a valuable addition for those seeking comprehensive protection against life-altering health events.

Guaranteed Insurability Rider

The guaranteed insurability rider enables policyholders to increase their life insurance coverage at specific intervals or life events—such as marriage, the birth of a child, or a mortgage increase—without requiring additional medical underwriting. Available for both term and permanent policies, this rider ensures coverage can adapt to evolving needs, offering peace of mind by securing future insurability even if health conditions worsen over time.

While it typically incurs an additional premium to provide this flexibility, the rider follows a straightforward structure and often includes predefined option dates or limits on additional coverage amounts, making it a valuable tool for those planning for long-term security and significant life milestones.

Long-Term Care Rider

The long-term care rider enhances a life insurance policy by enabling policyholders to access a portion of the death benefit early to cover expenses related to long-term care, such as nursing home care, in-home assistance, or assisted living, providing essential support during periods of extended health needs. Available for both term and permanent policies, this rider reduces the eventual death benefit by the amount withdrawn, offering a practical solution for managing care costs without depleting other savings.