Financial advisors can be compensated in various ways, and understanding these differences is key when choosing the right one for you. Whether an advisor is fee-only or fee-based can significantly influence the recommendations they provide. As a fee-only advisor, we’re committed to transparency and aligning our guidance with your best interests. We invite you to explore the distinctions between fee-only and fee-based models to make an informed decision when selecting your advisor.

TrustTas Capital is a....

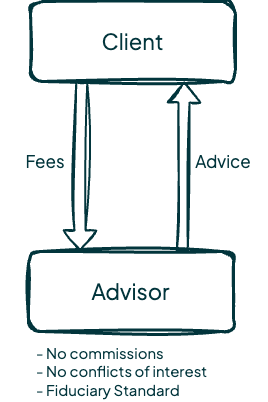

Fee-only Advisor

Fee-only Advisors

A fee-only advisor is compensated directly by the client through a transparent, straightforward method for their services. This approach eliminates commissions, referral fees, kickbacks, or any hidden forms of compensation, removing the inherent conflicts of interest that can arise when advisors sell insurance, mutual funds, annuities, or other financial products for a commission. Instead, fee-only advisors focus solely on providing the best possible financial advice, free from the pressure to push products.

A fee-only advisor is compensated directly by the client through a transparent, straightforward method for their services. This approach eliminates commissions, referral fees, kickbacks, or any hidden forms of compensation, removing the inherent conflicts of interest that can arise when advisors sell insurance, mutual funds, annuities, or other financial products for a commission. Instead, fee-only advisors focus solely on providing the best possible financial advice, free from the pressure to push products.

Fee-only advisors are typically compensated in one of these ways: (A) a percentage of the assets they manage for the client, (B) hourly fees, (C) project-based fees, or (D) ongoing retainer or subscription fees.

As fiduciaries, fee-only advisors are legally obligated to act in their clients’ best interests at all times. This duty requires full disclosure of any potential conflicts of interest and thorough analysis of investments before offering recommendations. Typically registered as investment advisors (RIAs) with the U.S. Securities and Exchange Commission (SEC) or state-level authorities, their compensation details are publicly accessible via Form ADV, allowing you to verify their fee structure with ease.

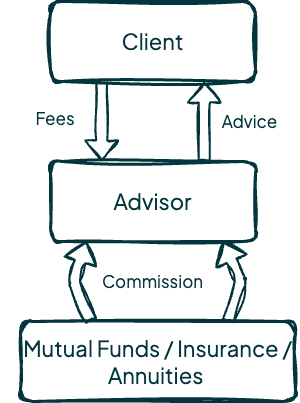

Fee-based Advisors

Fee-based advisors charge clients a fee for their services, much like fee-only advisors, but they also earn additional compensation through commissions on sales of mutual funds, annuities, insurance, and other financial products. This dual structure often makes it challenging for clients to fully understand the fees involved, which may include 12b-1 fees, surrender charges, back-end fees, contingency fees, wrap fees, soft-dollar benefits, and more. Even seemingly small fees can significantly erode your portfolio’s performance over time, making it critical to minimize unnecessary costs for long-term success.

Fee-based advisors charge clients a fee for their services, much like fee-only advisors, but they also earn additional compensation through commissions on sales of mutual funds, annuities, insurance, and other financial products. This dual structure often makes it challenging for clients to fully understand the fees involved, which may include 12b-1 fees, surrender charges, back-end fees, contingency fees, wrap fees, soft-dollar benefits, and more. Even seemingly small fees can significantly erode your portfolio’s performance over time, making it critical to minimize unnecessary costs for long-term success.

Ultimately, fee-based advisors face an inherent conflict of interest. Their incentive to sell products that generate commissions can lead to recommendations that are suitable but not necessarily optimal for you as a client.

Our Fees

At TrustTas Capital, we’ve structured our fees to prioritize our clients’ interests, ensuring transparency and simplicity. Neither TrustTas Capital nor its employees accept compensation from the sale of securities or financial products. Below, we outline the fee structures for our two core services.

Personal Financial Planning Fees

Since each client’s financial situation is unique, the complexity of each financial plan varies. Fees for financial planning are determined by TrustTas Capital after the initial client meeting, based on the intricacy of your circumstances. Typically, these services range from $600 to $1,200. The exact cost is detailed in your Financial Planning Agreement (FPA), providing full clarity on what you’ll pay.

Fees are negotiable and billed in full upon delivery of the final financial plan report. The FPA allows either party to terminate the agreement with written notice, provided termination occurs before the final plan is presented.

Wealth Management Fees

Our wealth management services are designed for clients seeking an ongoing financial partnership. TrustTas Capital is compensated through a retainer fee, set after completing your personal financial plan. These fees are negotiable but typically range from $50 to $100 per month (or $200 to $400 per quarter). Your Wealth Management Retainer Agreement (WMRA) will specify the exact amount.

The WMRA permits termination by either party with immediate effect upon written notice. Any prepaid, unearned fees—covering the full month or quarter of the notice date, regardless of when it’s received—will be refunded to you.

Other Fees & Expenses

Recommendations may include investments in mutual funds, ETFs, index funds, or other vehicles, each with its own separate fees. Transaction charges may also apply when you buy or sell securities. TrustTas Capital does not receive any portion of these fees, and we strive to minimize them in your best interest.

Additionally, based on your financial plan, we may recommend outside attorneys, accountants, or other specialized services, each with their own distinct fees.

FAQs

Are you a fee-only or fee-based advisor?

TrustTas Capital is a fee-only financial advisory firm. We believe this approach best prioritizes your interests, delivering guidance in a clear and transparent manner.

What are the main differences between fee-only and fee-based advisors?

Fee-only advisors are compensated exclusively by their clients, ensuring unbiased guidance. In contrast, fee-based advisors may earn additional income (such as commissions) from the investments they recommend, which can introduce potential conflicts of interest.

What is the major advantage of using a fee-only financial planner?

By choosing a fee-only financial advisor like TrustTas Capital, you engage a fiduciary legally obligated to prioritize your interests. This ensures you receive objective financial advice, untainted by external influences that could sway investment recommendations.

How are you compensated for your services?

We are compensated directly by you, our client. We offer two distinct services, and you can explore the details of our fee structure here →