Test

TrustTas Guiding Principles

Portfolio Construction

- T

- L

- H

- T

- C

- T

Overview

Open Architecture Investment Philosophy

An open-architecture investment philosophy prioritizes flexibility and customization over rigid, one-size-fits-all strategies. This approach allows our firm or yourself to evaluate each investment opportunity on its individual merits, free from the constraints of third-party products. Here at TrustTas Capital we maintain an unbiased and independent perspective, ensuring that our portfolio recommendations are driven solely by the potential to deliver value, aligning seamlessly with each client’s unique financial goals, risk tolerance, and investment horizon.

In practice, our open-architecture philosophy means we source and analyze investment options from a broad universe of opportunities and help clients with individual needs. We leverage rigorous due diligence and market insights to identify strategies that complement a client’s existing portfolio while addressing their specific objectives—whether that’s capital preservation, income generation, or long-term growth.

This client-centric approach fosters a dynamic and adaptive investment strategy. Rather than adhering to a static framework, we continuously monitor market conditions and have clients inform of us of evolving needs, adjusting allocation recommendations to optimize performance and mitigate risks. By integrating diverse asset classes and strategies, we aim to construct portfolios that are resilient, diversified, and positioned to capitalize on opportunities across market cycles.

Ultimately, our open-architecture philosophy empowers us to act as true fiduciaries, placing client interests at the forefront. By tailoring each portfolio recommendation to reflect individual priorities and leveraging a wide range of investment solutions, we strive to deliver superior outcomes that enhance wealth creation and financial security.

Emphasis On After-Tax Return

Maximizing after-tax returns is a fundamental pillar of to any portfolio construction process. Our firm recognizes that taxes can significantly diminish investment gains if not strategically managed, which is why tax efficiency is central to our recommendations. Our goal is to help clients retain more of their returns, aligning investment strategies with long-term wealth-building objectives.

Typically, we begin with a detailed assessment of each client’s tax profile—including income levels, capital gains exposure, and relevant tax regulations—to develop customized, tax-aware strategies that complement their investment goals and risk tolerance.

A core tactic is strategic asset location: allocating investments across taxable, tax-deferred, and tax-exempt accounts to enhance after-tax outcomes. For instance, we often advice placement of tax-inefficient assets—such as bonds or actively managed funds—within tax-advantaged accounts like IRAs, while reserving taxable accounts for tax-efficient holdings such as index funds or ETFs. This deliberate placement recommendation minimizes the tax drag on investment income and capital gains.

We may also recommend tax-loss harvesting, identifying opportunities to sell underperforming assets to offset realized gains elsewhere in the portfolio. When executed with precision, this approach can materially reduce taxable income without compromising the overall investment strategy. Additionally, we consider investment holding periods, with a preference for long-term capital gains, which are generally taxed at lower rates than short-term gains.

Our focus on after-tax return extends to the careful selection of investment vehicles. We favor tax-efficient instruments—such as exchange-traded funds (ETFs)—that tend to generate fewer taxable events compared to traditional mutual funds.

Finally, we remain vigilant to changes in tax policy, ensuring portfolios are continuously aligned with evolving regulations. By embedding tax planning into every stage of the investment process, we strive not only for portfolio growth but also for long-term wealth preservation in the most tax-efficient way possible. This comprehensive approach reflects our commitment to delivering meaningful, net-of-tax returns that support our clients’ financial goals.

Risk Mitigation

Effective risk management is an important principle to portfolio construction philosophy, ensuring your or our client’s portfolios are resilient against market volatility and aligned with individual risk tolerances. We employ a multifaceted approach to mitigate risks, with a particular focus on reducing unsystematic risk through diversification while addressing systematic risk through strategic asset allocation and advanced techniques. Our goal is to construct portfolios that balance risk and reward, safeguarding client wealth while pursuing consistent, long-term returns.

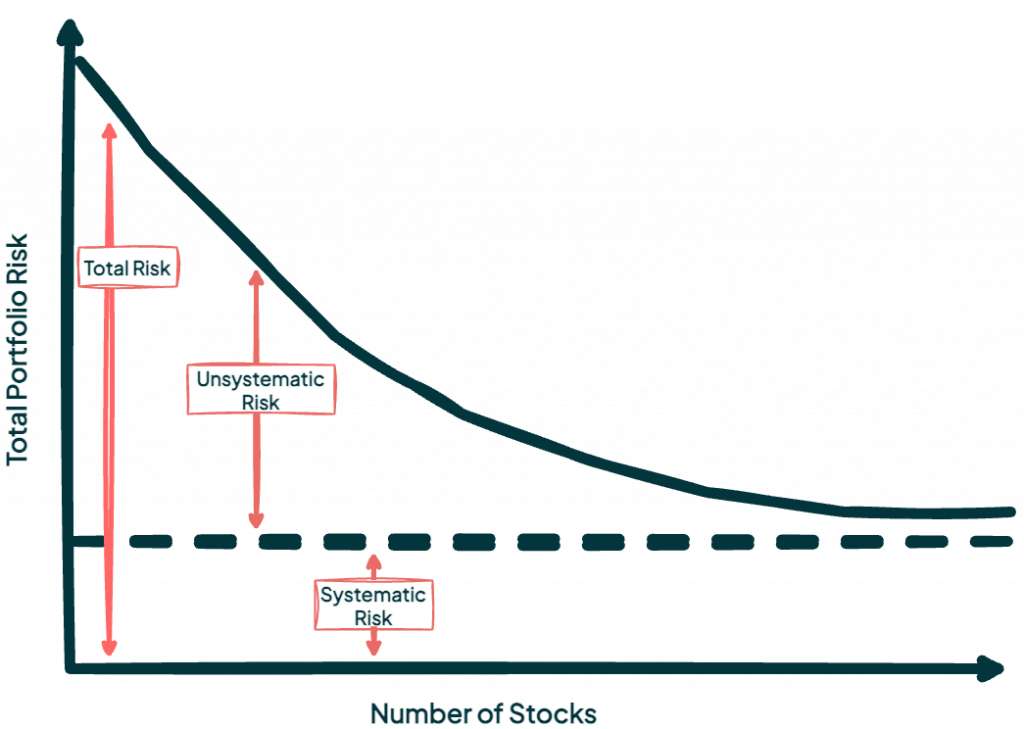

Diversify To Reduce Unsystematic Risk

Investment risks are broadly categorized into systematic and unsystematic risks. Systematic risk, driven by macroeconomic factors such as interest rate changes, inflation, or geopolitical events, affects the entire market and cannot be eliminated through diversification. Unsystematic risk, however, stems from factors specific to individual securities or sectors, such as company mismanagement or industry downturns, and can be significantly reduced through careful portfolio construction.

Diversification is the cornerstone to mitigate unsystematic risk. By spreading investments across a wide range of securities, sectors and asset classes, we minimize the impact of any single underperforming investment on the overall portfolio. For example, a portfolio holding stocks in diverse sectors—such as technology, healthcare, financials, and consumer staples—reduces the risk of sector-specific declines. Studies indicate that a well-diversified portfolio of 20–30 uncorrelated stocks can reduce unsystematic risk by up to 80%, as the idiosyncratic risks of individual securities offset one another.

Watch For Yield Curve Inversions

A critical component of our risk management strategy involves closely monitoring the yield curve, particularly for inversions, which can signal potential economic challenges and influence investment decisions. The yield curve, which plots the yields of government bonds across different maturities, typically slopes upward, reflecting higher yields for longer-term bonds due to increased risk and uncertainty over time. An inversion occurs when short-term yields exceed long-term yields, often indicating market expectations of economic slowdown or recession.

Historically, yield curve inversions—particularly between the 2-year and 10-year U.S. Treasury notes—have been reliable predictors of recessions, often preceding them by 12 to 24 months. This chart is shown below:

An inverted yield curve suggests that investors anticipate lower future growth and inflation, prompting demand for long-term bonds, which drives their yields below those of short-term bonds. This phenomenon can impact portfolio performance, as it may signal declining equity markets, tightening monetary policy, or reduced lending activity, all of which affect asset prices and economic conditions.

Our approach involves proactively monitoring yield curve dynamics to inform asset allocation and risk management. By recognizing early signs of inversion, we can adjust portfolio recommendations to mitigate potential downside risks while positioning for opportunities that may arise during economic transitions.

Strategic Responses to Yield Curve Inversions

When a yield curve inversion is detected, we suggest clients take several steps to safeguard their portfolios:

- Reduced Equity Exposure: In anticipation of potential market volatility, we may selectively advice clients to reduce exposure to high-beta or cyclical equities, favoring more stable-oriented investments.

- Enhanced Cash and Liquidity: An inverted yield curve may prompt us to recommend an increase cash holdings or investments in short-term, high-quality fixed-income securities to preserve capital and maintain flexibility during uncertain periods.

However, we avoid knee-jerk reactions and advice to yield curve inversions, recognizing that they are signals, not certainties. Our recommendation response is tailored to each client’s investment objectives and risk tolerance, ensuring that adjustments align with their long-term goals. For instance, a client with a long investment horizon may maintain a growth-oriented portfolio with minor tweaks, while a more conservative client might shift toward capital preservation strategies.

By vigilantly monitoring yield curve inversions and integrating these insights into our broader investment framework, we enhance our ability to navigate economic cycles effectively. This proactive stance strengthens portfolio resilience, helping clients weather potential downturns while remaining positioned for long-term success.

Keep Liquidity Needs In Cash

Maintaining adequate liquidity is key to our portfolio construction philosophy, ensuring clients have access to funds when needed without compromising the integrity of their long-term investment strategy. By keeping your liquidity needs in cash or cash-equivalent instruments, you provide a buffer for planned and unexpected expenses, enhance portfolio flexibility, and mitigate the risk of forced asset sales during unfavorable market conditions.

Liquidity refers to the ability to quickly access funds without incurring significant losses or transaction costs. For clients, liquidity needs may arise from planned expenses (e.g., major purchases, tax obligations, retirement distributions, etc.) or unforeseen circumstances (e.g., medical emergencies or income disruptions). Holding a portion of the portfolio in cash or highly liquid, low-risk assets ensures these needs can be met promptly, avoiding the need to sell longer-term investments at inopportune times, such as during market downturns when asset prices may be depressed.

Cash also serves as a risk management tool, providing stability and flexibility in volatile markets. It acts as a “dry powder” reserve, allowing clients to seize investment opportunities when markets present undervalued assets or to weather periods of economic uncertainty without disrupting their portfolio’s strategic allocation.

Determining Liquidity Needs

Our approach to liquidity begins with a thorough assessment of each client’s financial profile, including their income, expenses, investment horizon, and short-term cash flow requirements. We collaborate with clients to estimate both immediate and near-term liquidity needs, typically covering 12–36 months of anticipated expenses, depending on their circumstances. By tailoring liquidity allocations to individual needs, we ensure portfolios remain practical and responsive to real-world demands while preserving growth potential.

Focus On Risk Tolerance

The overarching goal of our portfolio construction recommendations is to align investments with each client’s unique risk tolerance, ensuring that portfolios reflect their comfort with market volatility while supporting their financial objectives. Risk tolerance—the degree to which an investor is willing and able to withstand fluctuations in portfolio value—varies widely based on individual circumstances, goals, and psychological preferences. By prioritizing risk tolerance, we create tailored portfolio recommendations that balance growth potential with stability, fostering confidence and long-term success.

Risk tolerance may not be static; as it may evolve with life events, market conditions, and changes in financial circumstances. A client’s risk appetite may shift due to major milestones (e.g., marriage, retirement, or inheritance), economic developments, or changes in personal confidence. We maintain an ongoing dialogue with clients to reassess their risk tolerance periodically, ensuring that their portfolio recommendations remain aligned with their current needs and preferences.

For example, a client approaching retirement may transition from a growth-oriented portfolio to one focused on income and capital preservation, reflecting a lower risk tolerance. Conversely, a young professional receiving a significant income increase may opt for a more aggressive strategy to accelerate wealth accumulation.

Understanding Risk Tolerance

Assessing risk tolerance is a critical first step in our investment process. We engage with clients to evaluate both their financial capacity to absorb losses and their emotional comfort with market uncertainty. Key factors influencing risk tolerance include:

- Financial Goals and Time Horizon: Clients with long-term objectives, such as saving for retirement decades away, may tolerate higher volatility for greater growth potential, while those nearing retirement or with short-term goals often prefer lower-risk investments.

- Income and Net Worth: Higher income or wealth may provide a greater buffer against losses, allowing for more aggressive strategies, whereas clients with limited resources may prioritize capital preservation.

- Investment Experience: Seasoned investors may be more comfortable with market swings, while novice investors may prefer more conservative approaches.

- Personal Preferences: Some clients are naturally risk-averse, favoring stability, while others are more risk-tolerant, willing to embrace volatility for higher potential returns.

We use a combination of detailed questionnaires, one-on-one discussions, and scenario analyses to quantify and understand each client’s risk tolerance. This ensures that our portfolio recommendations align with both their financial capacity and psychological comfort.

Educating and Empowering Clients

We believe that understanding risk is key to client confidence. We educate clients about the risks associated with different investments, providing clear explanations of potential outcomes and how our strategies may mitigate those risks. By fostering transparency and open communication, we empower clients to make informed decisions and feel secure in their investment journey.

By focusing on risk tolerance, we create personalized portfolio recommendations that not only align with each client’s financial goals but also provide peace of mind. This client-centric approach ensures that portfolios are resilient, adaptable, and designed to deliver sustainable returns within the boundaries of each investor’s comfort with risk.

Guard Against Inflation

Protecting portfolios from the erosive effects of inflation is a critical, ensuring that clients’ purchasing power is preserved over the long term. Inflation, the gradual increase in the price of goods and services, can significantly diminish the real value of investment returns if not addressed proactively. Our approach integrates equity strategies to mitigate inflation risk, aligning with clients’ financial goals while maintaining portfolio resilience across economic cycles.

Inflation erodes the purchasing power of money over time, meaning that a dollar today will buy less in the future. For investors, this translates to a need for returns that not only match but exceed the inflation rate to achieve real (inflation-adjusted) growth. For example, if inflation averages 3% annually and a portfolio returns 4% before inflation, the real return is only 1%. Over decades, even moderate inflation can significantly reduce wealth if not properly managed.

To guard against inflation, we recommend investing enough of the portfolio into equities. Stocks have historically outpaced inflation over long periods, making them a cornerstone of inflation-hedging strategies. While guarding against inflation is critical, we tailor our strategies to each client’s risk tolerance, time horizon, and financial objectives.

By integrating inflation-hedging strategies into our broader portfolio construction framework, we help clients preserve their purchasing power and achieve real wealth growth. Our proactive, client-centric approach ensures that portfolios are not only protected against inflation but also positioned to thrive in diverse economic environments.

Efficient Market Hypothesis

(EMH)

The Efficient Market Hypothesis (EMH), introduced by Eugene Fama in the 1960s, is central to modern financial theory, asserting that asset prices in financial markets fully incorporate all available information at any given moment. This implies that prices are always fair, making it challenging for investors to consistently outperform the market through stock selection or market timing. EMH’s profound influence shapes portfolio construction by guiding investors toward strategies that prioritize efficiency, diversification, and cost-effectiveness.

The theory also underpins several key financial models, including the Capital Asset Pricing Model (CAPM) and Modern Portfolio Theory (MPT), which assume that markets are efficient and that investors are rational in their decision-making.

While behavioral finance and market anomalies challenge the hypothesis, its principles continue to shape portfolio construction, promoting disciplined, evidence-based approaches to wealth creation. For most investors, adhering to EMH through passive investing offers a reliable path to achieving long-term financial goals. Understanding its principles is essential for building robust portfolios that align with the realities of competitive markets.

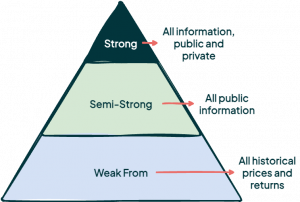

Hypothesis Exists In Three Forms

The hypothesis is categorized into three distinct forms, each reflecting a different level of market efficiency and the scope of information incorporated into asset prices. These forms provide a framework for understanding how information influences market behavior and the challenges investors face in attempting to outperform the market:

The hypothesis is categorized into three distinct forms, each reflecting a different level of market efficiency and the scope of information incorporated into asset prices. These forms provide a framework for understanding how information influences market behavior and the challenges investors face in attempting to outperform the market:

↳ Weak Form

The weak form of EMH states that all past price and volume information is fully reflected in current asset prices. This means that historical data, such as price trends, trading volumes, or chart patterns, cannot be used to predict future price movements or generate excess returns. As a result, technical analysis—strategies that rely on identifying patterns in historical price data, such as moving averages or support and resistance levels—is deemed ineffective in consistently outperforming the market.

The weak form assumes that markets efficiently process all historical information, leaving no exploitable patterns for investors to capitalize on. For example, a trader using past stock price trends to forecast future movements would find no consistent advantage, as any predictable patterns are already priced in.

↳ Semi-Strong Form

The semi-strong form of EMH expands the scope to include all publicly available information, such as financial statements, earnings reports, economic indicators, news releases, and analyst recommendations. According to this form, asset prices adjust rapidly to reflect new public information, rendering fundamental analysis—evaluating a company’s intrinsic value based on financial metrics like earnings, revenue, or debt—largely ineffective for achieving consistent outperformance.

For instance, when a company announces better-than-expected earnings, the stock price typically adjusts almost immediately as the market incorporates this information. The semi-strong form implies that investors cannot gain a sustained edge by analyzing public data, as the market’s efficiency ensures that such information is quickly and accurately reflected in prices. This challenges the value of extensive research into public financial data, as any insights gained are likely already accounted for in the market.

↳ Strong Form

The strong form of EMH is the most comprehensive, asserting that asset prices reflect all information—both public and private, including insider knowledge. Under this form, even privileged information, such as non-public details about corporate mergers or strategic decisions, is assumed to be fully incorporated into prices, making it impossible for any investor, including insiders, to achieve consistent excess returns.

This form suggests an idealized level of market efficiency where no information asymmetry exists, and prices are always perfectly aligned with all available knowledge. However, the strong form is the most controversial, as empirical evidence, such as profitable insider trading or delayed price reactions to private information, suggests that markets may not always incorporate non-public information instantaneously. For example, cases of insider trading prosecutions demonstrate that some individuals can exploit private information before it becomes public, challenging the strong form’s assumptions. Despite this, the strong form serves as a theoretical benchmark for understanding the upper limits of market efficiency.

Implications for Portfolio Construction

The Efficient Market Hypothesis (EMH) profoundly influences portfolio construction by shaping investment strategies, asset allocation decisions, and risk management practices. By assuming that asset prices reflect all available information, EMH encourages investors to adopt approaches that align with market efficiency, prioritize cost minimization, and focus on long-term objectives rather than speculative attempts to outperform the market.

1. Passive Investing and Index Funds

EMH’s assertion that markets are efficient and prices reflect fair value underpins the rise of passive investing. Since consistently outperforming the market is challenging, investors are better served by constructing portfolios that replicate broad market indices, such as the S&P 500. Index funds and exchange-traded funds (ETFs) provide low-cost, diversified exposure to the market, capturing its average return without the need for active stock selection or market timing.

For example, an investor building a portfolio around a total market index fund benefits from broad diversification, low expense ratios, and minimal turnover, aligning with EMH’s view that attempting to exploit mispricings is unlikely to yield consistent excess returns. Passive investing has grown significantly in popularity, with data showing that index funds often outperform actively managed funds over the long term, especially after accounting for fees.

2. Diversification

EMH emphasizes the importance of diversification to eliminate unsystematic risk—the risk specific to individual securities—since mispricings are rare in efficient markets. This aligns with Modern Portfolio Theory (MPT), which advocates for constructing portfolios that optimize the risk-return tradeoff. By spreading investments across a wide range of assets, investors can reduce the impact of idiosyncratic risks while capturing market-wide returns.

In an EMH framework, diversification ensures that a portfolio’s performance is driven by systematic risk (market risk) rather than the uncertain outcomes of individual securities. Investors construct portfolios along the efficient frontier, selecting asset combinations that maximize expected returns for a given level of risk, assuming that market prices are fair and reflect all available information.

3. Active Management Challenges

For investors who pursue active management, EMH presents significant hurdles. Active strategies, such as stock picking or market timing, rely on identifying mispriced securities or predicting market movements—tasks that EMH deems nearly impossible in efficient markets. Research consistently shows that most active managers fail to outperform their benchmarks after accounting for fees and transaction costs.

This evidence supports the EMH-driven preference for passive strategies, though some investors argue that inefficiencies may exist in less liquid or less transparent markets, such as small-cap stocks, emerging markets, or certain sectors. For instance, active managers may find opportunities in markets with lower analyst coverage, but these opportunities require significant skill and resources, making them inaccessible to most investors.

4. Risk-Adjusted Returns

EMH encourages investors to focus on risk-adjusted returns rather than chasing absolute returns, as expected returns are tied to systematic risk in efficient markets. The Capital Asset Pricing Model (CAPM), rooted in EMH, suggest that an asset’s expected return is a function of its beta, which measures its sensitivity to market movements. Portfolio construction under EMH involves selecting assets that align with an investor’s risk tolerance and investment objectives, ensuring that risk exposure is intentional and aligned with expected returns.

For example, an investor with a low risk tolerance might construct a portfolio with a lower beta, incorporating bonds or low-volatility equities, while a risk-tolerant investor might tilt toward higher-beta assets like growth stocks. EMH underscores that chasing outsized returns without considering risk is unlikely to succeed in an efficient market.

Modern Portfolio Theory

(MPT)

Investing can sometimes feel like navigating a maze, with countless options and unpredictable market movements. How do you choose the right mix of investments to grow your wealth while keeping risks manageable? Modern Portfolio Theory (MPT), developed by Harry Markowitz in the 1950s, offers a practical solution. MPT is a framework designed to help investors like you build portfolios that balance the potential for returns with the level of risk you’re comfortable taking.

At its heart, MPT is about diversification—spreading your investments across different assets, such as stocks, bonds, and real estate, to reduce risk while aiming for solid returns. It recognizes that no single investment is a magic bullet, but by carefully combining assets that behave differently, you can create a portfolio that performs well in various market conditions.

MPT starts with a simple but profound idea: risk and return go hand in hand. Higher returns often come with higher risks, but by diversifying your investments, you can reduce the impact of any single asset’s ups and downs. MPT uses math and data to find the optimal mix of investments, ensuring you get the most return for the risk you’re willing to take—or the least risk for the return you want.

This approach aligns with the idea that markets are generally efficient, meaning stock and bond prices reflect all available information. As a result, it’s tough to consistently “beat” the market by picking individual winners or timing trades perfectly. Instead, MPT focuses on creating a diversified portfolio that captures market returns efficiently, saving you time, stress, and costly mistakes.

Core Principles of MPT

Modern Portfolio Theory (MPT) revolutionized investing by offering a systematic way to build portfolios that balance the potential for growth with the risks you’re willing to take. Instead of chasing hot stocks or trying to time the market, MPT focuses on the big picture: constructing a portfolio that works efficiently to meet your financial goals. Its core principles provide a roadmap for making smarter investment decisions.

These ideas have shaped modern investing, influencing everything from index funds to robo-advisors. While MPT isn’t perfect—it assumes markets behave predictably and ignores real-world costs like taxes—it remains a cornerstone of portfolio construction, offering a timeless framework for balancing risk and reward.

1) Risk and Return Go Hand in Hand

MPT starts with a simple truth: higher potential returns come with higher risks. If you want your portfolio to grow significantly, you’ll likely need to accept some volatility. But MPT shows you don’t have to take unnecessary risks to achieve solid returns. By carefully selecting and combining investments, you can optimize your portfolio to get the highest return possible for the level of risk you’re comfortable with—or the lowest risk for your target return.

For example, imagine you’re choosing between a volatile stock market index (expected return of 8% with high swings) and a stable government bond (4% return with minimal volatility). MPT helps you decide how much to allocate to each based on your risk tolerance, ensuring you’re not overexposed to wild market swings or stuck with meager returns.

2) Diversification: Your Portfolio’s Safety Net

You’ve probably heard the advice, “Don’t put all your eggs in one basket.” MPT takes this to the next level by making diversification the heart of smart investing. Diversification means spreading your money across different asset classes—like stocks and bonds—that don’t move in perfect sync. When one asset takes a hit (say, stocks drop during a market crash), another might hold steady or even rise (like bonds), cushioning your portfolio’s overall performance. When one asset zigs, another might zag, smoothing out your portfolio’s overall performance.

The magic of diversification lies in correlation, a measure of how assets move relative to each other. Assets with low or negative correlations (e.g., stocks and bonds) are especially powerful for reducing risk without sacrificing too much return. For instance, during the 2008 financial crisis, stocks plummeted, but many government bonds held their value, protecting diversified portfolios. MPT uses math to find the right mix of assets, minimizing what’s called unsystematic risk (risk specific to individual investments) while keeping your expected returns on track.

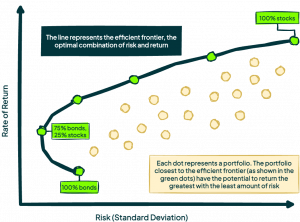

3. The Efficient Frontier: Finding the Optimal Portfolio

What’s the best portfolio for you? MPT answers this with the efficient frontier, a concept that represents the set of portfolios offering the highest expected return for a given level of risk—or the lowest risk for a desired return. Picture a graph where the x-axis shows risk (measured as standard deviation, or volatility) and the y-axis shows expected return. The efficient frontier is a curved line showing the “sweet spot” portfolios—no other combination of assets gives you a better tradeoff.

What’s the best portfolio for you? MPT answers this with the efficient frontier, a concept that represents the set of portfolios offering the highest expected return for a given level of risk—or the lowest risk for a desired return. Picture a graph where the x-axis shows risk (measured as standard deviation, or volatility) and the y-axis shows expected return. The efficient frontier is a curved line showing the “sweet spot” portfolios—no other combination of assets gives you a better tradeoff.

For example, a portfolio with 100% stocks might offer an 8% expected return but with high volatility (20% standard deviation). A 50-50 stock-bond mix might give a 6% return with only 10% volatility. MPT’s goal is to identify these efficient portfolios through mean-variance optimization, a process that uses expected returns, risks, and correlations to calculate the best asset weights. Investors can then pick a portfolio on the efficient frontier that matches their risk appetite—aggressive investors choose higher-risk, higher-return portfolios, while conservative ones opt for safer mixes.

The Math Behind It

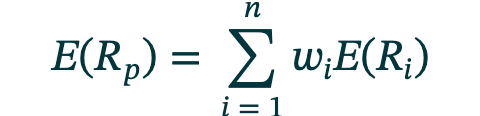

Expected Return of a Portfolio

The first piece of MPT’s math is calculating the expected return of a portfolio, which is the weighted average of the returns of its individual investments. For example, if you invest in stocks and bonds, the portfolio’s return depends on how much you allocate to each and their expected performance. The expected return of a portfolio formula is listed below:

- E(Rₚ) = Expected portfolio return

- wᵢ = Weight of asset i in the portfolio

- E(Rᵢ) = Expected return of asset i

- n = Number of assets

Example

Stock (Asset A): Represents a broad equity index (e.g., S&P 500).

- Expected return: E(Rₐ) = 7% (typical for equities over the long term).

- Standard deviation: σₐ=20% (reflecting equity volatility).

- Stock: wₐ=75%

Bond (Asset X): Represents a government bond (e.g., 10-year Treasury)

- Expected return: E(Rₓ) = 4% (typical for safe bonds).

- Standard deviation: σₓ=6% (bonds are less volatile).

- Stock: wₓ=25%

Bond & Stock Correlation

- ρₐₓ=0.2 (unchanged, as stocks and bonds typically have low positive correlation)

Expected Return

E(Rₚ) = (0.75 * 0.07) + (0.25 * 0.04) = .0525 + .01 = .0625 or 6.25%

Portfolio Risk (Volatility)

In MPT, risk is measured as the portfolio’s standard deviation, which captures the expected volatility of its returns. It accounts not only for the risk of each asset but also for how assets interact through their correlations. Portfolio risk (standard deviation) is calculated as:

- σₚ = Portfolio standard deviation

- wᵢwⱼ = Weights of assets i and j

- σᵢσⱼ = Standard deviations of assets i and j

- ᵢⱼ = Correlation coefficient between assets i and j

Example

Stock (Asset A): Represents a broad equity index (e.g., S&P 500).

- Expected return: E(Rₐ) = 7% (typical for equities over the long term).

- Standard deviation: σₐ=20% (reflecting equity volatility).

- Stock: wₐ=75%

Bond (Asset X): Represents a government bond (e.g., 10-year Treasury)

- Expected return: E(Rₓ) = 4% (typical for safe bonds).

- Standard deviation: σₓ=6% (bonds are less volatile).

- Bond: wₓ=25%

Bond & Stock Correlation

- ρₐₓ=0.2 (unchanged, as stocks and bonds typically have low positive correlation)

Variance of Stock (Asset A)

- wₐ² σₐ² = (0.75^2) * (0.20^2) = 0.5625 * 0.04 = 0.0225

Variance of Bond (Asset X)

- wₓ²σₓ² = (0.25^2) * (0.06^2) = .0625 * .0036 = 0.000225

Covariance Term

- σₐσₓρₐₓ=0.20 * 0.06 * 0.2 = 0.0024

- wₐwₓσₐσₓρₐₓ=

- Since the formula includes both i=1, j=2 and i=2, j=1, the total covariance contribution is 2 * wₐwₓσₐσₓρₐₓ = 2 * 0.00045 = 0.0009

Sum the Variance Components

- σ²=wₐ²σₐ²+wₓ²σₓ²+2wₐwₓσₐσₓρₐₓ = 0.0225 + 0.000225 + 0.0009 = 0.023625

- Take the square root of 0.023625 = 15.37%

Keep It Simple

Construct A Portfolio Using Passive Index Funds & ETFs

T

Focus On Asset Allocation

T

Dollar Cost Average

T

Keep Fees Low

T

Rebalance Annually

T

Advance

Passive, Leveraged ETFs

T

Tax Loss Harvesting

T

Asset Location Matters

T